Non-Resident Jumbo Mortgage Lenders

Jumbo and Super Jumbo No Resident Foreign National Florida Mortgage Lenders provide highly competitive interest rates. Flexible terms. Tailored options. Loan amounts up to $30 million or more. Jumbo and Super Jubmo loans can be the right fit when purchasing a luxury home or high-priced investment property.

|

|

|

|

Non-Resident Jumbo Mortgage Lenders For Non-Resident Foreign Nationals

A (NRA) non-resident alien is defined as a borrower who does not live and work in the U.S. This does not include permanent resident aliens or non-permanent resident aliens. If borrowers do not have a valid work VISA, or work authorization card, and live and work outside the U.S., they are considered non-resident aliens. In addition, non-resident aliens are limited to loans on second home or non-owner-occupied transactions. The following list contains the most common work visas that indicate a Due Diligence review is required (note, this list is not exhaustive): • B-1, B-2 • BBBCV, C1 • E-1, E-2, EB, EB-5 • NAFTA • O, O-1, • P-1, P-2, P-3 •

Temporary Green Card

o Borrowers from countries participating in the State Department’s VISA Waiver Program (VWP) are not required to provide a valid visa.

NOTE: additional documents may be requested as part of the Due Diligence review when there are NRA loans with gift funds (either from U.S. citizens or NRAs), and/or when there are NRA Title Holders or NRA Beneficial Owners.

All NRA loans are submitted for NRA Due diligence review and this is required before submission to underwriting. This may take a few days and require additional information. If approved the file will be submitted to Credit for an initial underwriting decision. The review fee is $250.

Additional Requirements:

• Copy of SSN or unexpired ITIN card

• Valid passport

• Valid VISA

o If the bank statements reflect significant asset amounts that are not necessarily commensurate with the underwritten income (e.g. $10 million balance in bank but employment pays $80,000 per year), a Letter of Explanation from the borrower explaining the source of their wealth is required by BSA

• Amounts not denominated in U.S. dollars must be converted to USD

• A minimum of 12 months PITIA is required in reserves;

• Thorough online research of borrower name and business is required;

• Professional translation of all income/identity/asset documentation if not in

Required:

• Research country of origin;

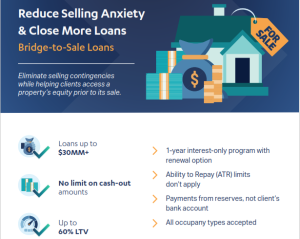

• NRA Borrowers are not eligible for the Bridge to Sale Loan Program Program Exclusions

• Applicants with diplomatic immunity are not allowed;

• POAs are not allowed;

• Vesting in an entity is allowed, but no part of the entity can be foreign

Income Documents:

Two years tax returns are required from the Country of Origin, if tax returns are filed in that country. They must be translated by a 3rd party professional translation company. Convert all currency into USD. If tax returns are NOT required, then one or more of the following items of documentation may be obtained:

• CPA (or equivalent) letter verifying income,

• Paystubs or pay statements

• Letter from employer

All must be translated by a 3rd party professional translation company. Convert all currency into U.S. Dollar (“USD”). A 25% Discount for Foreign Currency Conversion Risk is applied to calculated qualifying monthly income.

Foreign Credit Reports:

Credit reports will be obtained using a valid Social Security number or Individual Tax Payer Identification Number (ITIN).

o Minimum credit score: 680

o Pricing and credit review based of lowest middle score No FICO score is allowed if borrower(s) provide evidence of credit history through non-traditional credit references covering a minimum of two (2) open tradelines reporting for two (2) years with activity in the most recent 12 months.

• Housing payment history required (mortgage or rental history)

• Utilities

• Banking relationships

• Credit Cards

• Cell phone payments

• Insurance payment

Primary Residence Expenses:

Every NRA loan should include expenses for the primary residence such as rental payments, mortgage, taxes, insurance HOA dues and any other applicable expenses.

Assets: Assets should be verified with two months’ statements from the borrower’s accounts. If the statements are not in English, they must be translated by a 3rd party professional translation company. Convert all currency into USD. All foreign gift funds should be approved—all donors’ identities, sources of the funds, and employment require such clearance. The Bank will consider gifted funds from a maximum of 5 giftors and none may be, or have any affiliation with, the builder, developer, real estate agent, mortgage banker/broker, or any other interested party to the transaction.

Additional documents: US Mailing address must be provided for mailing of monthly statements

Jumbo and Super Jumbo Florida Mortgage Options Include:

-

Bridge-to-Sale – Help clients access their listed property’s equity before its sale.

-

Bank Statement– Use multiple income streams for qualification, including personal or business bank statements.

- Foreign National – Non-Resident– Jumbo Super Jumbo refinance up to 15 MM with CPA letter on independent CPA firm’s company letterhead properly dated.

- Asset Depletion– Increase client purchasing power by calculating assets into qualifying income, without liquidating.

- Cross-Collateralization– Access Jumbo home equity to purchase a new home without having to sell first. Cashout up to 100% of a home’s value by securing the loan against an additional free and clear property.

- Condo Condotel – Super Jumbo Condo and Condotel Florida mortgage lenders for Unique properties.

-

Pledged Asset – Leverage assets (stocks, mutual funds, etc.) without liquidating. Jumbo cashouts up to 90% of a home’s value by pledging security assets or savings.

-

DSCR– Jumbo DSCR loans for investment properties using only 1007 rental income to qualify.

- Bad Credit Florida Jumbo Mortgage– Jumbo mortgage exceptions with unforeseen circumstances.