Jumbo Florida Bridge Lenders – Bridge Lenders For Luxury Florida Homes

A Florida Jumbo bridge loan is a short-term financing option, also known as a swing loan or gap loan, used to bridge the gap between selling an existing luxury Florida property and purchasing a new one or to cover short-term financing needs until a permanent jumbo mortgage loan is secured. In the right situation when a jumbo Florida mortgage applicant doesn’t want to wait for the sale of another luxury property and would like to avoid contingencies, or seeks to gain a competitive edge a bridge loan can be an option.

Bridge Loans Alleviate the “buy-before-you-sell” Issue.

The stress of coordinating the buying and selling transactions can be eliminated with a jumbo Florida bridge loan. Instead, the buyer can focus on purchasing the property they want without the restrictions of having to sell their old property first.

Jumbo bridge loans give luxury Florida mortgage applicants time to move into a new home, get settled, and then focus on selling the old one. When moving to a new community, this type of loan can alleviate the need for a buyer to temporarily rent a property while waiting for the old home to sell.

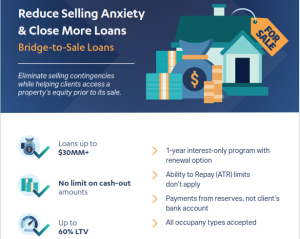

Bridge Loan Summary

Common Use Cases: Buying a new luxury Florida home before selling the current one.

Alternatives: Using the equity in a current luxury home to finance a new purchase, but this is not an option if the current home is for sale.

Characteristics: Jumbo Florida Bridge loans are typically short-term, with repayment usually expected within 24 months.

Florida Jumbo and Super Jumbo Loans

Jumbo and Super Florida Jumbo Loans offer the flexibility of borrowing with fewer restrictions. They can be used to finance primary residences, second or vacation Florida homes, and investment properties. A Jumbo Loan may also be the right option when refinancing an existing home loan or consolidating multiple mortgages into a single loan.

A mortgage is generally considered a Jumbo Loan when it exceeds the conforming loan limit, $726,200 in most U.S counties, set by Fannie Mae and Freddie Mac. Super Jumbo Loans usually include mortgage amounts over $1 million.

What is the benefit of a residential jumbo Florida bridge loan?

Without a large financial cushion, many jumbo mortgage applicants don’t have enough money to make a down payment on a new home before the sale of their old home. A bridge loan is used to span the time between the purchase of the new property and the sale of the old property.

The loans are often set up in two ways. One option is for the loan to be large enough to pay off the mortgage on the old home and be used for a down payment on the new home.

Another option is to use the loan only for a down payment on the new home. The collateral for the loan is often the home that is for sale. When the home sells, most jumbo mortgage applicants use the proceeds to pay off the bridge loan.

A bridge loan may be useful for several reasons:

- Removes contingencies from the equation.

- Provides increased leverage in a competitive housing market.

- Alleviates the “sell-before-you-buy” dilemma.

How do Florida Jumbo bridge loans work?

Florida bridge loans are short-term loans offered by select banks and bridge loan Florida mortgage lenders. They typically last for at least 12 months but can often be extended up to 24 months. These bridge loans can be structured in different ways depending on the jumbo Florida mortgage applicant’s need.

Bridge loans are available for both residential and commercial real estate purchases. They may not require minimum credit scores and debt-to-income ratios, as Florida bridge loan lenders focus more on the loan’s viability and the jumbo Florida mortgage applicant’s ability to repay it.

Interest rates on bridge loans are often higher than average fixed-rate jumbo Florida mortgage products, usually by around 2%. However, the rates can vary widely along with the loan terms and fees. jumbo Florida mortgage applicants might get better rates and terms if they obtain the bridge loan and the long-term mortgage from the same lender.

Payment structure can also vary by lender. At, we collect 12 months of payments upfront, which is then held in a deposit account. Interest-only payments are then made from this account for the term of the loan. A balloon payment is then made at the end of the term or when the property sells.

Increased leverage in a competitive Florida housing market.

In a competitive housing market, a bridge loan can allow the buyer to move swiftly with an offer. If the seller is prioritizing a quick sale, a jumbo Florida mortgage applicant who can move forward immediately without waiting for their old property to sell often has leverage over other buyers.

Removes jumbo Florida mortgage quaifying contingencies from the equation.

Another advantage of a bridge loan is that it allows the buyer to avoid a contingent offer that relies on the sale of another property. This can put the buyer at a disadvantage because many sellers won’t accept a contingent offer of this type. Removing this contingency through a bridge loan can make the buyer’s offer more attractive.

Weighing the Rewards vs. Risks of a Jumbo Florida Bridge Loan

Bridge loans offer both benefits and risks. The main risk is that the jumbo Florida mortgage applicant’s old property might not sell within the loan term. However, this can be mitigated by having a binding contract of sale on the old property.

Researching the local housing market can help Florida jumbo mortgage applicants make an informed decision by understanding the average time it takes homes to sell. Negotiating a 6-month extension on the bridge loan may be an option based on the findings.

Jumbo Florida mortgage applicants may find they obtain better terms when working with a single Jumbo Floria mortgage lender instead of using two different lenders. The jumbo Florida mortgage applicant will want to carefully review all the terms of the loan and understand if there are prepayment penalties.

Florida Bridge loan substitutes

There are many options outside of a Jumbo Florida bridge loan. Two that don’t require the sale of investments for a down payment include a Home Equity Line of Credit and the use of pledged assets. A third option is cross-collateralization, which uses the equity from an existing property that the jumbo Florida mortgage applicant doesn’t immediately plan to sell.

Jumbo Florida Home Equity Line of Credit (HELOC)

If a jumbo Florida mortgage applicant has significant equity in the old property, a HELOC could be an option. Based on the Jumbo Florida mortgage applicant’s maximum draw amount, they may be able to use the available money from their HELOC for the down payment on the new home. However, this is not an option if the old property is listed for sale.

In most cases, the jumbo Florida mortgage applicant will need an existing HELOC or will want to apply for one before putting their house on the market. Few lenders will give jumbo mortgage applicants a line of credit once the property is on the market.

Jumbo Florida Mortgage a Down Payment with Pledged Assets

A less common down payment option is a pledged asset mortgage. It allows a jumbo Florida mortgage applicant to leverage their stocks and liquid assets to help lower the loan-to-value ratio (LTV) of their new mortgage.

Instead of a larger down payment, the jumbo Florida mortgage applicant pledges assets such as stocks, bonds, CDs, savings, or mutual funds to use as collateral on the loan. Because the jumbo Florida mortgage applicant isn’t making a down payment, they pay interest on the full price of the property.

Jumbo Florida Cross-Collateralization To Increase Buying Power

If a jumbo Florida mortgage applicant doesn’t have near-term plans to sell their existing property, they can also explore a cross-collateralization loan. This is a portfolio mortgage program that allows the jumbo Florida mortgage applicant to add a second property as collateral for a mortgage.

The result is one loan for the two homes. The extra equity minimizes the amount of cash that’s needed for a downpayment. If desired, the jumbo Florida mortgage applicant can later sell one of the properties or refinance to remove the additional home from the loan.

Jumbo and Super Jumbo Florida Mortgage Options Include:

-

Bridge-to-Sale – Help clients access their listed property’s equity before its sale.

- Condo Condotel – Super Jumbo Condo and Condotel Florida mortgage lenders for Unique properties.

-

Pledged Asset – Leverage assets (stocks, mutual funds, etc.) without liquidating. Jumbo cashouts up to 90% of a home’s value by pledging security assets or savings.

-

DSCR– Jumbo DSCR loans for investment properties using only 1007 rental income to qualify.

- Bad Credit Florida Jumbo Mortgage– Jumbo mortgage exceptions with unforeseen circumstances.

-

Bank Statement– Use multiple income streams for qualification, including personal or business bank statements.

- Foreign National – Non-Resident– Jumbo Super Jumbo refinance up to 15 MM with CPA letter on independent CPA firm’s company letterhead properly dated.

- Asset Depletion– Increase client purchasing power by calculating assets into qualifying income, without liquidating.

- Cross-Collateralization– Access Jumbo home equity to purchase a new home without having to sell first. Cashout up to 100% of a home’s value by securing the loan against an additional free and clear property.