No Income Verification Florida Investor Loans!

DSCR loans, or Debt Service Coverage Ratio loans are a type of no-income verification investor loan that is attractive to real estate investors because they can use the subject property’s current or projected income to qualify without using the borrower’s income to qualify. Basically, the qualifying income is based on the cash flow generated by the investment.

Why choose our DSCR?

- Minimum 600+ Credit score.

- No income and no employment are needed.

- Use Subject Properties Rental Income To Qualify.

- With a large enough Downpayment and/or equity almost any property with qualify.

- Faster turn times!

How does the lender know if a property has positive Cash Flow?

All DSCR lenders will require the investor to provide t a standard appraisal to verify the value allowed with appraisal Form 1007, the Single-Family Comparable Rent Schedule, is to be used by Florida mortgage lenders to estimate the market rent of the subject property. Adjustments should be made only for items of significant difference between the comparables and the subject property. Form 1007 is only to be used for conventional single-family investment properties and is to be included and prepared by the appraiser as an attachment to the uniform residential appraisal for the property. The market rent value is determined by analyzing three rental properties that share or bracket significant rental characteristics with the subject property, as well as information relating to the physical structure, location, and lease terms of the single-family property.

1. Focus on Properties Income:

DSCR loans primarily focus on the income potential of the property itself. This is a huge advantage for Florida investors who may have fluctuating incomes, are self-employed, or have income streams that are difficult to document traditionally. Easier Qualification: Instead of scrutinizing personal tax returns and W-2s, lenders assess the property’s projected rental income. This can make it easier to qualify for a loan, even if your financial picture is complex.

2. Streamlined Approval Process:

Because the focus is on the property’s income, the approval process for DSCR loans can be significantly faster than for traditional mortgages. This is because the property’s income after expenses is the main factor for approval.

3. Flexibility in Property Types:

DSCR loans can often be used to finance a variety of property types, including single-family homes, multi-family units, and even commercial properties.

4. Potential for Higher Loan Amounts:

Case by case investors can borrow more with a DSCR loan than they could with a traditional mortgage, as the loan amount is tied to the property’s income potential, not the borrower’s financial situation.

5. No Limit on Number of Properties:

Unlike some traditional Florida mortgages, DSCR loans often don’t have limits on the number of properties you can finance. This can be a significant advantage for investors looking to build a larger portfolio.

About DSCR Florida Mortgage Lenders

Debt service coverage ratio Florida mortgage lenders use an alternative method to qualify investment property for the purchase or refinance of Florida real estate. Rather than using the borrower’s income via W2, 1099, and Tax Returns to verify the borrower’s ability to pay. (DSCR) debt service coverage ratio lenders use the rental income from the subject property to qualify instead of using the borrower’s ability to repay. The DSCR or debt service coverage ratio shows the amount of rental income you have every month after paying the total housing payment that includes PITI and HOA.

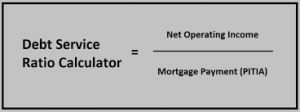

How Do You Calculate (the DSCR) Debt Service Coverage?

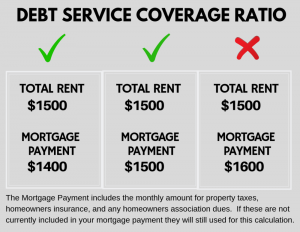

The DSCR is calculated by taking net operating income and dividing it by total debt service (which includes the principal and interest payments on a loan). For example, if a rental home has an income of $2000 per month and the total housing payment that includes Principal, Interest, Taxes, Insurance, and HOA is $1900 the DCR 2000/1900 = DSCR would be approximately 1.052. The lender is looking a number over 1 to approve your loan request.

What Is a Good DSCR Ratio?

A “good” DSCR for mortgage qualifying is any number greater than 1.00. As a general rule, however, a DSCR above 1.00 shows the property will generate enough income to cover the total housing payments. Most DSCR Florida mortgage lenders require at least 1 to qualify!

How to qualify for a DSCR mortgage in Florida?

Qualifying for a California DSCR loan is not difficult when you have the right property and meet other requirements. Here are general things lenders are looking for.

Loan purpose: Purchase a property, refinance (for instance, you could refinance out of a hard money loan), or cash-out refinance.

Property types allowed: Single-family residences, multi-family 2-4 unit homes, condos, non-warrantable condos, townhomes, and more. These loans also work for commercial properties, such as 5-8 unit apartment complexes and office buildings, although the DSCR calculation is different than for residential.

Loan-to-value (LTV): Maximum loan-to-value is typically 75-80%. For a purchase, this is the same as saying you need a 20-25% down payment. For a refinance, you have to have 20-25% equity.

Credit score: Case by case 500+.

Property use: Investment properties only; no primary residences. Short-term rentals are accepted.

Loan type: 30-year fixed, adjustable rate, and interest-only loans.

Income and employment, debt-to-income ratio: No personal income or DTI verification is required.

Maximum loan amount: Typically $1-2 million, but some lenders go up to $5 million or more.

Maximum properties owned: There’s no limit to the number of owned or financed properties.

Prepayment penalties: Many DSCR loans come with prepayment penalties. Make sure you intend to keep the home and mortgage until the penalty time period expires.

Closing in the name of an LLC: This is allowed.

Seller paid closing costs: Typically allowed up to a certain percentage of the home price.

Other Pages You May Be Interested in Include:

- NO Income Verification Investor Loans: Use the subject property’s income to qualify for your next investment property mortgage.

- Foreign National Mortgage Lenders: Nonresidents in the United States can invest using our FN mortgage options to purchase or cash out.

- Commercial mortgage Lenders: Case-by-case mortgage options for Florida office buildings, shopping centers, and warehouses.

- Reverse Mortgage Condo Lenders: 55+ Florida Condo owners can withdraw cash out of their condos without monthly mortgage payments.

- Bad Credit Florida Mortgage Lenders: Bad Credit based on a common sense approach based on payment history, not credit score driven.

- NO tax return Mortgage Lenders: Non-QM and Private Lenders offer alternative documentation options for mortgage qualifying.

- 1099 Only Mortgage Lenders: Use 1099 Income up to 100% income can be used with no verified business expenses.

- VOE Florida Mortgage Lenders: Private Florida Mortgage Lenders will allow your VOE to disregard your tax return write-offs.

- Bank Statement Mortgage Lenders: Use 12 or 24-month average bank deposits for mortgage income qualifying.

- Asset-Based Mortgage Lenders– Assets in your account to cover the purchase price qualify you for enough income to qualify.

- Self-Employed Mortgage Options – If you write off too much of your income to qualify for the necessary funds.

- P&L Only Mortgage Lenders: Use Your licensed Tax preparer to provide a profit and loss statement for mortgage income verification.