Florida Co-op Mortgage Lenders Serving All Florida

Refinance Purchase Jumbo Florida Coop Mortgage Florida. When you purchase or refinance a Florida coop or co-op you purchase shares in the corporation that owns the property. All coop owners in the building are shareholders and share in the expenses and maintenance of the property. And, when you purchase a co-op you purchase shares of the corporation that owns the building. So in reality you are a shareholder in the corporation, versus a typical homeowner. With a Co-op, each participant is a shareholder and gets to occupy a unit in the condo or housing complex. Co-op are often funded by non-qm mortgage lenders and private mortgage lenders because Fannie Mae does not purchase coop loans in Florida.

Coop Florida Mortgage Lenders For Warrantable and Non-Warrantable Florida Coops

|

Mortgage Options Include:

|

Minimum Loan Amount:

|

|

Loan to Value

|

Debt to Income Ratio (“DTI”):Max 50% DTI Ratio. |

|

Document Checklist

|

Borrower Eligibility:

|

Co-op Florida Mortgage Document Checklist:

3 Documents Needed To Get the building Approved first!

- Questionnaire – Call Us at 954-667-9110 to request a copy of the Florida co-op questionnaire.

- Master Insurance policy – Building-wide policy covering common areas and the building structure.

- Budget – Needed to operate and maintain includes utilities, insurance, and staff salaries, as well as improvements.

Co-op Restrictions

•Title Insurance policy issued through a title company or closing attorney must be issued on the Co-op certificate.

•Borrower paid attorney review of all applicable co-op documents or other pertinent items required before funding

•Leaseholds allowed with 30 years or more remaining on lease.

Co-op Reserve Requirements:

The current reserve balance meets or exceeds 2 months of the subject property’s HOA dues in reserves multiplied by all units in the project or 10% or more reserve allocation designated in the most recent budget.

Not allowed:

- NO Co-op Manufactured Homes

- No Structural deficiencies or pending litigation

- Incomplete construction of the subject phase

- Units without a stovetop and oven – must have both

- Homeowners Association with No reserves

- Homeowners Association limits the number of days the property can be accessed

Co-op Questions And Answers

Q –What Cities Do you Offer Co-op Loans in? Florida Coop Lenders in all of Florida including Palm Beach, Fort Lauderdale, Hallandale, Panama City, Naples, Clearwater, Gainesville, Jacksonville, Miami, Tampa, Orlando, St. Petersburg, Tallahassee, Port St. Lucie, Sarasota, Fort Myers, Daytona Beach, Sunny Isles, Bal Harbor, Aventura, Key Biscayne, juno beach, North Miami, and everywhere in Florida.

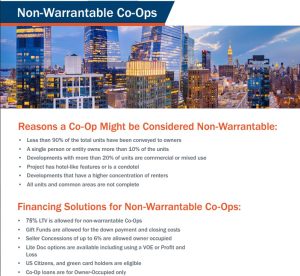

Q – Do we approve loans in coop projects that have re-sale, age, income, or any other owner-related restrictions?

A – Florida Coop with any sort of re-sale restrictions presents a severely negative impact on the marketability of the unit in the event the borrower defaults and this becomes an REO. It is important to identify what the restrictions are to determine project warrant ability and eligibility:

- If the only restriction is the “Right of First Refusal”, this is okay and the project can still be eligible as Warrantable.

- For projects with age restrictions, such as 55-and-older communities, we will allow financing to these projects as long as:

- Borrower meets the age requirements, and;

- The project must not have any rehabilitation, medical treatment, or elder-care facilities (for example, nursing homes).

- The project will only be considered eligible as a Non-Warrantable. If both the above conditions are not met, the loan will be ineligible under all loan programs.

- For projects with income restrictions, such as low-to-moderate income (LMI), we will allow financing to these projects as long as:

- the subject unit is NOT one of the LMI or income-restricted units.

- The project will only be considered eligible as a Non-Warrantable. If the above condition is not met, the loan will be ineligible under all loan programs.

- For all other re-sale or owner-related restrictions not identified above, the loan will be deemed ineligible under all loan programs.

Q- Does Fannie Mae Buy Co-op loans from lenders in Florida?

A – On the Fannie Mae it says they will fund loans in Florida but when I ask Florida mortgage lenders why they don’t make these loans they say that NO coops in Florida meet Fannie Mae’s specifications. This is why most Florida coop loans are harder to come by and funded only by private non-QM Florida mortgage lenders.

Florida Co-op Subdivision/Complex

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE HUNDRED SOUTH OCEAN | Caribe Co-Op Caribe Co-Op |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | Coral Ridge Towers East Coral Ridge Towers East |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | THREE EIGHTY NINE CORP LE | SANDPIPER VILLAS CO-OP SANDPIPER VILLAS |

| Coral Ridge Towers South Coral Ridge Towers South | LAKE DRIVE CO-OP APTS INC | Royal Saxon |

| Atlantic Towers Atlantic Towers | MURANO GRANDE AT PORTOFIN Murano Grande | OCEAN CLUB 1 |

| OASIS-NURMI ISLE CO-OP The Oasis | PARK PLACE INC | Coral Ridge Towers East Coral Ridge Towers East |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | ATLANTIC TOWERS CO-OP Atlantic Towers |

| BAY HARBOR CLUB CO-OP Bay Harbor Club Co-Op | The Elser Residences The Elser Residences | SEA CLUB OF HILLSBORO BEA |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | OKAN TOWER OKAN TOWER | Sea Tower Sea Tower |

| Paradise Harbour Paradise Harbour | PARAMOUNT BAY CONDO Paramount Bay | Breakwater Towers Breakwater Towers |

| CORAL COVE CORAL COVE | TWENTY TWO NINETY FIVE SO | Palm Beach Shores Apartme |

| COLONIAL RIDGE CORP | PALM HILL OCEAN CLUB CO-O | Atlantic Towers Atlantic Towers |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | REGENCY OF PALM BEACH INC | Villa Sorrento Villa Sorrento |

| 1446 OCEAN DR CO-OP APTS 1446 OCEAN DR | COVE BEACH CLUB COVE BEACH CLUB | CROSSWINDS CROSSWINDS |

| ISLE OF PARADISE CO-OP ISLE OF PARADISE CO-OP | PALM WORTH INC | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP |

| FAIRBANKS TERRACE SOUTH C FAIRBANKS TERRACE SOUTH C | AMBASSADOR II CORP | Crosswinds Crosswinds |

| CoralRidge Tower Original CoralRidge Tower Original | TWENTY TWO NINETY FIVE SO | Coral Ridge Towers North Coral Ridge Towers North |

| Coral Ridge Towers North Coral Ridge Towers North | Harbour House |

CORAL RIDGE TOWERS EAST Coral Ridge Towers East

|

| LAKEVIEW LODGE CO-OP LAKEVIEW LODGE CO-OP | AMBASSADOR SOUTH DEV CORP | 1750 Las Olas Co-op 1750 Las Olas Co-op |

| PARADISE TOWERS CO-OP Paradise Towers | AMBASSADOR SOUTH DEV CORP | OCEANA SOUTH CONDOMINIUM |

| TIFFANY APTS CO-OP Tiffany Apts Co-Op | AMBASSADOR II CORP | SEA CLUB OF HILLSBORO BEA |

| RIVIERA APTS RIVIERA APTS | ISLAND HOUSE APT INC – CO Island House |

CORAL RIDGE TOWERS CO-OP CORAL RIDGE TOWERS CO-OP

|

| Coral Ridge Towers South Coral Ridge Towers South | FONTAINEBLEAU III OCEAN C SORRENTO | LA FONTANA APTS OF PALM B |

| SHEFFIELD WOODS AT WELLIN Sheffield Woods at Wellin | AMBASSADOR II CORP | CULMER VILLAS CULMER VILLAS PB 106-50 |

| Beach Breeze Beach Breeze | 2295 SOUTH OCEAN BLVD COR | BOCA GRANADA WEST INC |

| BAY HARBOR CLUB CO-OP Bay Harbor Club | THE PLAZA 851 BRICKELL CO The Plaza on Brickell | Coral Ridge Towers East Coral Ridge Towers East |

| COSTA HOLLYWOOD CONDO COSTA HOLLYWOOD CONDO | GROSVENOR HOUSE INC | LEISURE BEACH CONDO LEISURE BEACH CONDO |

| COASTAL WATERWAYS CO-OP Coastal Waterways Co-Op | ISLAND HOUSE APT INC -COOP ISLAND HOUSE APT INC-COOP | LA BONNE VIE CONDO |

| Lexington Arms Co-Op Lexington Arms Co-Op | Old Port Cove – Lake Poin | BREAKWATER TOWERS CO-OP |

| PARADISE HARBOUR APTS CO- Paradise Harbour | AMBASSADOR | Norfolk House Norfolk House |

| Marine Colony Villas Marine Colony Villas | Versailles Versailles | CORAL RIDGE TOWERS EAST C |

| CARIBE CARIBE | REGENCY OF PALM BEACH INC | IMPERIAL WESTBURY CO-OP IMPERIAL WESTBURY |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Delrado | BREAKWATER TOWERS CO-OP Breakwater Towers |

| FAIRBANKS TERRACE SOUTH | Delrado | IMPERIAL HOUSE INC |

| Coral Ridge Towers Coral Ridge Towers | Orleans Chateau & Villas Orleans Chateau & Villas |

HILLSBORO MILE OCEAN APTS HILLSBORO MILE OCEAN APTS

|

| Coral Ridge Towers South Coral Ridge Towers South | VIRGINIA KAYE CO-OP Virginia Kaye | Coral Ridge Towers East Coral Ridge Towers East |

| The Oasis-Nurmi Isle The Oasis-Nurmi Isle | BAL HARBOUR RES SEC Bal Bridge South | EDGEWATER ARMS CO-OP EDGEWATER ARMS CO-OP |

| DELRAY COLONIAL | BURLEIGH HOUSE CONDO Burleigh House | RIVIERA APTS A INC OF HAL Riviera A |

| FAIRBANKS TERRACE SOUTH C Fairbanks Terrace | Cove Beach Club Cove Beach Club | Coral Ridge Towers Coral Ridge Towers |

| KENNEDY HOUSE CONDO KENNEDY HOUSE | Versailles Versailles |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| OCEAN BEACH FLA SUB Balmoral Apartments | TWENTY TWO NINETY FIVE SO | Hawthorne East Hawthorne East |

| GOLDEN BAY TOWERS CO-OP Golden Bay Towers | LEGENDS CONDO | VILLAS ON THE OCEAN |

| COASTAL WATERWAYS CO-OP coastal waterways | GOLDEN BAY TOWERS | OLYMPUS CONDO PHASE Olympus |

| CORAL RIDGE TOWERS CORAL RIDGE TOWERS | 4111 SOUTH OCEAN DRIVE CO 4111 SOUTH OCEAN DRIVE CO | Sea Tower Sea Tower |

| Coral Ridge Towers North Coral Ridge Towers North | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Harbor House Harbor House |

| Coral Ridge Towers Coral Ridge Towers | Spring Tide Apartments Spring Tide Apartments | Atlantic Towers Atlantic Towers |

| Coral Ridge Towers North Coral Ridge Towers North | Venice Venice | OYSTER BAY COOPERATIVE IN |

| ATLANTIC TOWERS ATLANTIC TOWERS | TWENTY TWO NINETY FIVE SO | ATLANTIC TOWERS ATLANTIC TOWERS |

| Breakwater Towers Breakwater Towers | TWENTY TWO NINETY-FIVE SO | Coral Ridge Towers South Coral Ridge Towers South |

| Colonial Ridge Corp | THE MERIDIAN CONDO The Meridian Condo |

SEA CLUB OF HILLSBORO BEA SEA CLUB OF HILLSBORO BEA

|

| Colonial Ridge Corp | REGENCY OF PALM BEACH INC | Coral Ridge Towers Coral Ridge Towers |

| LAKE COLONY APTS TWO INC | Lighthouse Colony Lighthouse Colony | LIGHTHOUSE COLONY CO-OP |

| PEN-TEN APTS INC CO-OP PEN-TEN APTS INC CO-OP | Regency at Boca Pointe | VILLAS ON THE OCEAN |

| Coral Ridge Towers Co-Op Coral Ridge Towers Co-Op | BOULAN SOUTH BEACH CONDO BOULAN SOUTH BEACH CONDO | Sea Tower Sea Tower |

| Coral Ridge Towers Coral Ridge Towers | Atlantic Towers Atlantic Towers |

WOODRIDGE AT CALFORNIA CL WOODRIDGE AT CALFORNIA CL

|

| Coral Ridge Towers East Coral Ridge Towers East | VIA VENTURE NEIGHBORHOOD VIA VENTURE NEIGHBORHOOD | LIGHTHOUSE COVE AT TEQUES |

| Villa Sorrento Villa Sorrento | EDGEWATER ARMS CO-OP | Breakwater Towers Breakwater Towers |

| THE MEADOWS LAKE NORTH CON THE MEADOWS LAKE NORTH CO | ISLE OF PARADISE CO-OP ISLE OF PARADISE | ISLANDER CO-OP ISLANDER CO-OP |

| Cypress Lake East Cypress Lake East | VIRGINIA KAYE CO-OP VIRGINIA KAYE CO-OP |

CORAL RIDGE TOWERS EAST C CORAL RIDGE TOWERS

|

| OPTIMA VILLAGE OPTIMA VILLAGE | ALAQUA CONDO ALAQUA | Coral Ridge Towers Coral Ridge Towers |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | LA FONTANA APTS OF PALM B | PALMBEACHER APTS INC |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Fort Lauderdale Surf Club Fort Lauderdale Surf Club | COLONIAL RIDGE CORP |

| Fairbanks Terrace South Fairbanks Terrace South | Oasis Nurmi Isle |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| BREAKWATER TOWERS CO-OP BREAKWATER TOWERS | CANVAS CONDO CANVAS CONDO | CoralRidge Tower Original CoralRidge Tower Original |

| Lake Mayan Apartments Lake Mayan Apartments | El Dorado Club El Dorado Club | PALMBEACHER |

| MARINE TERRACE CO-OP marine terrace | CORAL RIDGE SOUTH CO-OP CORAL RIDGE SOUTH CO-OP | COLONIAL RIDGE CORP |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Coral Ridge Tower South Coral Ridge Tower South | Breakwater Towers Breakwater Towers |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Spring Tide Apartment Spring Tide Apartment | BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP |

| OCEAN TERRACE CO-OP APTS Ocean Terrace | LAFAYETTE ARMS CO-OP LAFAYETTE ARMS | PARADISE TOWERS CO-OP PARADISE TOWERS |

| ISLE OF PARADISE CO-OP Isle Of Paradise | JAMAICA MANOR INC LESSEE | Coral Ridge Towers South Coral Ridge Towers South |

| Coral Ridge Towers East Coral Ridge Towers East | Ambassador II |

CROSSWINDS APTS INC CO-OP Crosswinds Co-Op Comm

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | OPERA TOWER CONDO OPERA TOWER CONDO |

CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH

|

| Cypress Lake #9 Co-Op Cypress Lake #9 Co-Op | ROYAL SAXON INC | alagon alagon |

| SUNSET VILLAS NO 3 CONDO SUNSET VILLAS CONDO | ATLANTIC TOWERS CO-OP Atlantic Towers | Coral Ridge Towers East Coral Ridge Towers East |

| MARINE TERRACE CO-OP | VIRGINIA KAYE | CARLTON BAY CONDO CARLTON BAY CONDO |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS | Hillsboro Ocean Apts. Hillsboro Ocean Apts. | KING COLE CONDO KING COLE CONDO |

| CASA PARADISO CO-OP Casa Paradiso | Riviera Towers Riviera Towers | ASHLEIGH HOUSE CONDO ASHLEIGH HOUSE CONDO |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | CAPRI CO-OP CAPRI CO-OP | ANDORIC APTS CO-OP Andoric Apartments |

| Coral Ridge Towers East Coral Ridge Towers East | PALMBEACHER APTS INC | CRANE CREST APTS CO-OP Crane Crest |

| CoralRidge Tower Original CoralRidge Tower Original | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP | Coral Ridge Towers Coral Ridge Towers |

| Cypress Island Cypress Island | Coral Ridge Towers North Coral Ridge Towers North | COLONIAL RIDGE CORP |

| W & C CONDO W & C CONDO | 1060 BRICKELL CONDO 1060 Brickell | Silver Shores Silver Shores |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | TAROMINA CO-OP Taromina | SEA COLONY CO-OP SEA COLONY CO-OP |

| THE ESQUIRE HOUSE OF M B THE ESQUIRE CONDO | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Coral Ridge Towers North Coral Ridge Towers North |

| THE ESQUIRE HOUSE OF M B Esquire House of Miami Be | ROYAL SAXON INC | Coral Ridge Towers Coral Ridge Towers |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS CO-OP | AMBASSADOR II | Coral Ridge Towers East Coral Ridge Towers East |

| COASTAL WATERWAYS CO-OP Coastal Waterways | CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH | GLENS CONDO |

| CASA PARADISO CO-OP CASA PARADISO | FOXGLOVE CO-OP FOXGLOVE | IMPERIAL HOUSE INC |

| Q CLUB RESORT & RESIDENCE QClub Resort and Residenc | Edgerwater arms Edgerwater arms | VILLAS ON THE OCEAN |

| Cypress Island Cypress Island | LAMIL SUB Monterey Villas | ROYAL SAXON INC |

| LAKE COLONY APTS THREE IN | REGENCY OF PALM BEACH INC | Atlantic Towers Co-op Atlantic Towers Co-op |

| ANDORIC APARTMENTS ANDORIC APARTMENTS | Estates at Acqualina Estates at Acqualina | MYSTIC POINTE TOWER 500 C Mystic Pointe Tower |

| SEA CLUB OF HILLSBORO BEA | VILLAS INC | Breakwater Towers Breakwater Towers |

| Coral Ridge Towers Coral Ridge Towers | DORCHESTER INC 200 N OCEA | Coral Ridge Towers Coral Ridge Towers |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE EIGHTY NINE CORP LE |

APEX AT PARK CENTRAL COND APEX AT PARK CENTRAL COND

|

| Coral Ridge Towers North Coral Ridge Towers North | Aston Martin Aston Martin Residences | Royal Saxon Inc |

| HILLSBORO MILE OCEAN APTS | THREE EIGHTY NINE CORP LE | Breakwater Towers Breakwater Towers |

| Colonial Ridge Club | SOMERSET OF GULFSTREAM IN | 518 Condo 518 Euclid Av 518 EUCLID |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP | THREE EIGHTY NINE CORP LE |

SIAN OCEAN RESIDENCES CON SIAN OCEAN RESIDENCES

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | PARK PLACE INC | Hawthorne House Hawthorne House |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE HUNDRED SOUTH OCEAN | Caribe Co-Op Caribe Co-Op |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | Coral Ridge Towers East Coral Ridge Towers East |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | THREE EIGHTY NINE CORP LE | SANDPIPER VILLAS CO-OP SANDPIPER VILLAS |

| Coral Ridge Towers South Coral Ridge Towers South | LAKE DRIVE CO-OP APTS INC | Royal Saxon |

| Atlantic Towers Atlantic Towers | MURANO GRANDE AT PORTOFIN Murano Grande | OCEAN CLUB 1 |

| OASIS-NURMI ISLE CO-OP The Oasis | PARK PLACE INC | Coral Ridge Towers East Coral Ridge Towers East |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | ATLANTIC TOWERS CO-OP Atlantic Towers |

| BAY HARBOR CLUB CO-OP Bay Harbor Club Co-Op | The Elser Residences The Elser Residences | SEA CLUB OF HILLSBORO BEA |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | OKAN TOWER OKAN TOWER | Sea Tower Sea Tower |

| Paradise Harbour Paradise Harbour | PARAMOUNT BAY CONDO Paramount Bay | Breakwater Towers Breakwater Towers |

| CORAL COVE CORAL COVE | TWENTY TWO NINETY FIVE SO | Palm Beach Shores Apartme |

| COLONIAL RIDGE CORP | PALM HILL OCEAN CLUB CO-O | Atlantic Towers Atlantic Towers |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | REGENCY OF PALM BEACH INC | Villa Sorrento Villa Sorrento |

| 1446 OCEAN DR CO-OP APTS 1446 OCEAN DR | COVE BEACH CLUB COVE BEACH CLUB | CROSSWINDS CROSSWINDS |

| ISLE OF PARADISE CO-OP ISLE OF PARADISE CO-OP | PALM WORTH INC | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP |

| FAIRBANKS TERRACE SOUTH C FAIRBANKS TERRACE SOUTH C | AMBASSADOR II CORP | Crosswinds Crosswinds |

| CoralRidge Tower Original CoralRidge Tower Original | TWENTY TWO NINETY FIVE SO | Coral Ridge Towers North Coral Ridge Towers North |

| Coral Ridge Towers North Coral Ridge Towers North | Harbour House |

CORAL RIDGE TOWERS EAST Coral Ridge Towers East

|

| LAKEVIEW LODGE CO-OP LAKEVIEW LODGE CO-OP | AMBASSADOR SOUTH DEV CORP | 1750 Las Olas Co-op 1750 Las Olas Co-op |

| PARADISE TOWERS CO-OP Paradise Towers | AMBASSADOR SOUTH DEV CORP | OCEANA SOUTH CONDOMINIUM |

| TIFFANY APTS CO-OP Tiffany Apts Co-Op | AMBASSADOR II CORP | SEA CLUB OF HILLSBORO BEA |

| RIVIERA APTS RIVIERA APTS | ISLAND HOUSE APT INC – CO Island House |

CORAL RIDGE TOWERS CO-OP CORAL RIDGE TOWERS CO-OP

|

| Coral Ridge Towers South Coral Ridge Towers South | FONTAINEBLEAU III OCEAN C SORRENTO | LA FONTANA APTS OF PALM B |

| SHEFFIELD WOODS AT WELLIN Sheffield Woods at Wellin | AMBASSADOR II CORP | CULMER VILLAS CULMER VILLAS PB 106-50 |

| Beach Breeze Beach Breeze | 2295 SOUTH OCEAN BLVD COR | BOCA GRANADA WEST INC |

| BAY HARBOR CLUB CO-OP Bay Harbor Club | THE PLAZA 851 BRICKELL CO The Plaza on Brickell | Coral Ridge Towers East Coral Ridge Towers East |

| COSTA HOLLYWOOD CONDO COSTA HOLLYWOOD CONDO | GROSVENOR HOUSE INC | LEISURE BEACH CONDO LEISURE BEACH CONDO |

| COASTAL WATERWAYS CO-OP Coastal Waterways Co-Op | ISLAND HOUSE APT INC -COOP ISLAND HOUSE APT INC-COOP | LA BONNE VIE CONDO |

| Lexington Arms Co-Op Lexington Arms Co-Op | Old Port Cove – Lake Poin | BREAKWATER TOWERS CO-OP |

| PARADISE HARBOUR APTS CO- Paradise Harbour | AMBASSADOR | Norfolk House Norfolk House |

| Marine Colony Villas Marine Colony Villas | Versailles Versailles | CORAL RIDGE TOWERS EAST C |

| CARIBE CARIBE | REGENCY OF PALM BEACH INC | IMPERIAL WESTBURY CO-OP IMPERIAL WESTBURY |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Delrado | BREAKWATER TOWERS CO-OP Breakwater Towers |

| FAIRBANKS TERRACE SOUTH | Delrado | IMPERIAL HOUSE INC |

| Coral Ridge Towers Coral Ridge Towers | Orleans Chateau & Villas Orleans Chateau & Villas |

HILLSBORO MILE OCEAN APTS HILLSBORO MILE OCEAN APTS

|

| Coral Ridge Towers South Coral Ridge Towers South | VIRGINIA KAYE CO-OP Virginia Kaye | Coral Ridge Towers East Coral Ridge Towers East |

| The Oasis-Nurmi Isle The Oasis-Nurmi Isle | BAL HARBOUR RES SEC Bal Bridge South | EDGEWATER ARMS CO-OP EDGEWATER ARMS CO-OP |

| DELRAY COLONIAL | BURLEIGH HOUSE CONDO Burleigh House | RIVIERA APTS A INC OF HAL Riviera A |

| FAIRBANKS TERRACE SOUTH C Fairbanks Terrace | Cove Beach Club Cove Beach Club | Coral Ridge Towers Coral Ridge Towers |

| KENNEDY HOUSE CONDO KENNEDY HOUSE | Versailles Versailles |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| OCEAN BEACH FLA SUB Balmoral Apartments | TWENTY TWO NINETY FIVE SO | Hawthorne East Hawthorne East |

| GOLDEN BAY TOWERS CO-OP Golden Bay Towers | LEGENDS CONDO | VILLAS ON THE OCEAN |

| COASTAL WATERWAYS CO-OP coastal waterways | GOLDEN BAY TOWERS | OLYMPUS CONDO PHASE Olympus |

| CORAL RIDGE TOWERS CORAL RIDGE TOWERS | 4111 SOUTH OCEAN DRIVE CO 4111 SOUTH OCEAN DRIVE CO | Sea Tower Sea Tower |

| Coral Ridge Towers North Coral Ridge Towers North | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Harbor House Harbor House |

| Coral Ridge Towers Coral Ridge Towers | Spring Tide Apartments Spring Tide Apartments | Atlantic Towers Atlantic Towers |

| Coral Ridge Towers North Coral Ridge Towers North | Venice Venice | OYSTER BAY COOPERATIVE IN |

| ATLANTIC TOWERS ATLANTIC TOWERS | TWENTY TWO NINETY FIVE SO | ATLANTIC TOWERS ATLANTIC TOWERS |

| Breakwater Towers Breakwater Towers | TWENTY TWO NINETY-FIVE SO | Coral Ridge Towers South Coral Ridge Towers South |

| Colonial Ridge Corp | THE MERIDIAN CONDO The Meridian Condo |

SEA CLUB OF HILLSBORO BEA SEA CLUB OF HILLSBORO BEA

|

| Colonial Ridge Corp | REGENCY OF PALM BEACH INC | Coral Ridge Towers Coral Ridge Towers |

| LAKE COLONY APTS TWO INC | Lighthouse Colony Lighthouse Colony | LIGHTHOUSE COLONY CO-OP |

| PEN-TEN APTS INC CO-OP PEN-TEN APTS INC CO-OP | Regency at Boca Pointe | VILLAS ON THE OCEAN |

| Coral Ridge Towers Co-Op Coral Ridge Towers Co-Op | BOULAN SOUTH BEACH CONDO BOULAN SOUTH BEACH CONDO | Sea Tower Sea Tower |

| Coral Ridge Towers Coral Ridge Towers | Atlantic Towers Atlantic Towers |

WOODRIDGE AT CALFORNIA CL WOODRIDGE AT CALFORNIA CL

|

| Coral Ridge Towers East Coral Ridge Towers East | VIA VENTURE NEIGHBORHOOD VIA VENTURE NEIGHBORHOOD | LIGHTHOUSE COVE AT TEQUES |

| Villa Sorrento Villa Sorrento | EDGEWATER ARMS CO-OP | Breakwater Towers Breakwater Towers |

| THE MEADOWS LAKE NORTH CON THE MEADOWS LAKE NORTH CO | ISLE OF PARADISE CO-OP ISLE OF PARADISE | ISLANDER CO-OP ISLANDER CO-OP |

| Cypress Lake East Cypress Lake East | VIRGINIA KAYE CO-OP VIRGINIA KAYE CO-OP |

CORAL RIDGE TOWERS EAST C CORAL RIDGE TOWERS

|

| OPTIMA VILLAGE OPTIMA VILLAGE | ALAQUA CONDO ALAQUA | Coral Ridge Towers Coral Ridge Towers |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | LA FONTANA APTS OF PALM B | PALMBEACHER APTS INC |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Fort Lauderdale Surf Club Fort Lauderdale Surf Club | COLONIAL RIDGE CORP |

| Fairbanks Terrace South Fairbanks Terrace South | Oasis Nurmi Isle |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| BREAKWATER TOWERS CO-OP BREAKWATER TOWERS | CANVAS CONDO CANVAS CONDO | CoralRidge Tower Original CoralRidge Tower Original |

| Lake Mayan Apartments Lake Mayan Apartments | El Dorado Club El Dorado Club | PALMBEACHER |

| MARINE TERRACE CO-OP marine terrace | CORAL RIDGE SOUTH CO-OP CORAL RIDGE SOUTH CO-OP | COLONIAL RIDGE CORP |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Coral Ridge Tower South Coral Ridge Tower South | Breakwater Towers Breakwater Towers |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Spring Tide Apartment Spring Tide Apartment | BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP |

| OCEAN TERRACE CO-OP APTS Ocean Terrace | LAFAYETTE ARMS CO-OP LAFAYETTE ARMS | PARADISE TOWERS CO-OP PARADISE TOWERS |

| ISLE OF PARADISE CO-OP Isle Of Paradise | JAMAICA MANOR INC LESSEE | Coral Ridge Towers South Coral Ridge Towers South |

| Coral Ridge Towers East Coral Ridge Towers East | Ambassador II |

CROSSWINDS APTS INC CO-OP Crosswinds Co-Op Comm

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | OPERA TOWER CONDO OPERA TOWER CONDO |

CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH

|

| Cypress Lake #9 Co-Op Cypress Lake #9 Co-Op | ROYAL SAXON INC | alagon alagon |

| SUNSET VILLAS NO 3 CONDO SUNSET VILLAS CONDO | ATLANTIC TOWERS CO-OP Atlantic Towers | Coral Ridge Towers East Coral Ridge Towers East |

| MARINE TERRACE CO-OP | VIRGINIA KAYE | CARLTON BAY CONDO CARLTON BAY CONDO |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS | Hillsboro Ocean Apts. Hillsboro Ocean Apts. | KING COLE CONDO KING COLE CONDO |

| CASA PARADISO CO-OP Casa Paradiso | Riviera Towers Riviera Towers | ASHLEIGH HOUSE CONDO ASHLEIGH HOUSE CONDO |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | CAPRI CO-OP CAPRI CO-OP | ANDORIC APTS CO-OP Andoric Apartments |

| Coral Ridge Towers East Coral Ridge Towers East | PALMBEACHER APTS INC | CRANE CREST APTS CO-OP Crane Crest |

| CoralRidge Tower Original CoralRidge Tower Original | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP | Coral Ridge Towers Coral Ridge Towers |

| Cypress Island Cypress Island | Coral Ridge Towers North Coral Ridge Towers North | COLONIAL RIDGE CORP |

| W & C CONDO W & C CONDO | 1060 BRICKELL CONDO 1060 Brickell | Silver Shores Silver Shores |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | TAROMINA CO-OP Taromina | SEA COLONY CO-OP SEA COLONY CO-OP |

| THE ESQUIRE HOUSE OF M B THE ESQUIRE CONDO | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Coral Ridge Towers North Coral Ridge Towers North |

| THE ESQUIRE HOUSE OF M B Esquire House of Miami Be | ROYAL SAXON INC | Coral Ridge Towers Coral Ridge Towers |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS CO-OP | AMBASSADOR II | Coral Ridge Towers East Coral Ridge Towers East |

| COASTAL WATERWAYS CO-OP Coastal Waterways | CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH | GLENS CONDO |

| CASA PARADISO CO-OP CASA PARADISO | FOXGLOVE CO-OP FOXGLOVE | IMPERIAL HOUSE INC |

| Q CLUB RESORT & RESIDENCE QClub Resort and Residenc | Edgerwater arms Edgerwater arms | VILLAS ON THE OCEAN |

| Cypress Island Cypress Island | LAMIL SUB Monterey Villas | ROYAL SAXON INC |

| LAKE COLONY APTS THREE IN | REGENCY OF PALM BEACH INC | Atlantic Towers Co-op Atlantic Towers Co-op |

| ANDORIC APARTMENTS ANDORIC APARTMENTS | Estates at Acqualina Estates at Acqualina | MYSTIC POINTE TOWER 500 C Mystic Pointe Tower |

| SEA CLUB OF HILLSBORO BEA | VILLAS INC | Breakwater Towers Breakwater Towers |

| Coral Ridge Towers Coral Ridge Towers | DORCHESTER INC 200 N OCEA | Coral Ridge Towers Coral Ridge Towers |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE EIGHTY NINE CORP LE |

APEX AT PARK CENTRAL COND APEX AT PARK CENTRAL COND

|

| Coral Ridge Towers North Coral Ridge Towers North | Aston Martin Aston Martin Residences | Royal Saxon Inc |

| HILLSBORO MILE OCEAN APTS | THREE EIGHTY NINE CORP LE | Breakwater Towers Breakwater Towers |

| Colonial Ridge Club | SOMERSET OF GULFSTREAM IN | 518 Condo 518 Euclid Av 518 EUCLID |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP | THREE EIGHTY NINE CORP LE |

SIAN OCEAN RESIDENCES CON SIAN OCEAN RESIDENCES

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | PARK PLACE INC | Hawthorne House Hawthorne House |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE HUNDRED SOUTH OCEAN | Caribe Co-Op Caribe Co-Op |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | Coral Ridge Towers East Coral Ridge Towers East |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | THREE EIGHTY NINE CORP LE | SANDPIPER VILLAS CO-OP SANDPIPER VILLAS |

| Coral Ridge Towers South Coral Ridge Towers South | LAKE DRIVE CO-OP APTS INC | Royal Saxon |

| Atlantic Towers Atlantic Towers | MURANO GRANDE AT PORTOFIN Murano Grande | OCEAN CLUB 1 |

| OASIS-NURMI ISLE CO-OP The Oasis | PARK PLACE INC | Coral Ridge Towers East Coral Ridge Towers East |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | ATLANTIC TOWERS CO-OP Atlantic Towers |

| BAY HARBOR CLUB CO-OP Bay Harbor Club Co-Op | The Elser Residences The Elser Residences | SEA CLUB OF HILLSBORO BEA |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | OKAN TOWER OKAN TOWER | Sea Tower Sea Tower |

| Paradise Harbour Paradise Harbour | PARAMOUNT BAY CONDO Paramount Bay | Breakwater Towers Breakwater Towers |

| CORAL COVE CORAL COVE | TWENTY TWO NINETY FIVE SO | Palm Beach Shores Apartme |

| COLONIAL RIDGE CORP | PALM HILL OCEAN CLUB CO-O | Atlantic Towers Atlantic Towers |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | REGENCY OF PALM BEACH INC | Villa Sorrento Villa Sorrento |

| 1446 OCEAN DR CO-OP APTS 1446 OCEAN DR | COVE BEACH CLUB COVE BEACH CLUB | CROSSWINDS CROSSWINDS |

| ISLE OF PARADISE CO-OP ISLE OF PARADISE CO-OP | PALM WORTH INC | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP |

| FAIRBANKS TERRACE SOUTH C FAIRBANKS TERRACE SOUTH C | AMBASSADOR II CORP | Crosswinds Crosswinds |

| CoralRidge Tower Original CoralRidge Tower Original | TWENTY TWO NINETY FIVE SO | Coral Ridge Towers North Coral Ridge Towers North |

| Coral Ridge Towers North Coral Ridge Towers North | Harbour House |

CORAL RIDGE TOWERS EAST Coral Ridge Towers East

|

| LAKEVIEW LODGE CO-OP LAKEVIEW LODGE CO-OP | AMBASSADOR SOUTH DEV CORP | 1750 Las Olas Co-op 1750 Las Olas Co-op |

| PARADISE TOWERS CO-OP Paradise Towers | AMBASSADOR SOUTH DEV CORP | OCEANA SOUTH CONDOMINIUM |

| TIFFANY APTS CO-OP Tiffany Apts Co-Op | AMBASSADOR II CORP | SEA CLUB OF HILLSBORO BEA |

| RIVIERA APTS RIVIERA APTS | ISLAND HOUSE APT INC – CO Island House |

CORAL RIDGE TOWERS CO-OP CORAL RIDGE TOWERS CO-OP

|

| Coral Ridge Towers South Coral Ridge Towers South | FONTAINEBLEAU III OCEAN C SORRENTO | LA FONTANA APTS OF PALM B |

| SHEFFIELD WOODS AT WELLIN Sheffield Woods at Wellin | AMBASSADOR II CORP | CULMER VILLAS CULMER VILLAS PB 106-50 |

| Beach Breeze Beach Breeze | 2295 SOUTH OCEAN BLVD COR | BOCA GRANADA WEST INC |

| BAY HARBOR CLUB CO-OP Bay Harbor Club | THE PLAZA 851 BRICKELL CO The Plaza on Brickell | Coral Ridge Towers East Coral Ridge Towers East |

| COSTA HOLLYWOOD CONDO COSTA HOLLYWOOD CONDO | GROSVENOR HOUSE INC | LEISURE BEACH CONDO LEISURE BEACH CONDO |

| COASTAL WATERWAYS CO-OP Coastal Waterways Co-Op | ISLAND HOUSE APT INC -COOP ISLAND HOUSE APT INC-COOP | LA BONNE VIE CONDO |

| Lexington Arms Co-Op Lexington Arms Co-Op | Old Port Cove – Lake Poin | BREAKWATER TOWERS CO-OP |

| PARADISE HARBOUR APTS CO- Paradise Harbour | AMBASSADOR | Norfolk House Norfolk House |

| Marine Colony Villas Marine Colony Villas | Versailles Versailles | CORAL RIDGE TOWERS EAST C |

| CARIBE CARIBE | REGENCY OF PALM BEACH INC | IMPERIAL WESTBURY CO-OP IMPERIAL WESTBURY |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Delrado | BREAKWATER TOWERS CO-OP Breakwater Towers |

| FAIRBANKS TERRACE SOUTH | Delrado | IMPERIAL HOUSE INC |

| Coral Ridge Towers Coral Ridge Towers | Orleans Chateau & Villas Orleans Chateau & Villas |

HILLSBORO MILE OCEAN APTS HILLSBORO MILE OCEAN APTS

|

| Coral Ridge Towers South Coral Ridge Towers South | VIRGINIA KAYE CO-OP Virginia Kaye | Coral Ridge Towers East Coral Ridge Towers East |

| The Oasis-Nurmi Isle The Oasis-Nurmi Isle | BAL HARBOUR RES SEC Bal Bridge South | EDGEWATER ARMS CO-OP EDGEWATER ARMS CO-OP |

| DELRAY COLONIAL | BURLEIGH HOUSE CONDO Burleigh House | RIVIERA APTS A INC OF HAL Riviera A |

| FAIRBANKS TERRACE SOUTH C Fairbanks Terrace | Cove Beach Club Cove Beach Club | Coral Ridge Towers Coral Ridge Towers |

| KENNEDY HOUSE CONDO KENNEDY HOUSE | Versailles Versailles |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| OCEAN BEACH FLA SUB Balmoral Apartments | TWENTY TWO NINETY FIVE SO | Hawthorne East Hawthorne East |

| GOLDEN BAY TOWERS CO-OP Golden Bay Towers | LEGENDS CONDO | VILLAS ON THE OCEAN |

| COASTAL WATERWAYS CO-OP coastal waterways | GOLDEN BAY TOWERS | OLYMPUS CONDO PHASE Olympus |

| CORAL RIDGE TOWERS CORAL RIDGE TOWERS | 4111 SOUTH OCEAN DRIVE CO 4111 SOUTH OCEAN DRIVE CO | Sea Tower Sea Tower |

| Coral Ridge Towers North Coral Ridge Towers North | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Harbor House Harbor House |

| Coral Ridge Towers Coral Ridge Towers | Spring Tide Apartments Spring Tide Apartments | Atlantic Towers Atlantic Towers |

| Coral Ridge Towers North Coral Ridge Towers North | Venice Venice | OYSTER BAY COOPERATIVE IN |

| ATLANTIC TOWERS ATLANTIC TOWERS | TWENTY TWO NINETY FIVE SO | ATLANTIC TOWERS ATLANTIC TOWERS |

| Breakwater Towers Breakwater Towers | TWENTY TWO NINETY-FIVE SO | Coral Ridge Towers South Coral Ridge Towers South |

| Colonial Ridge Corp | THE MERIDIAN CONDO The Meridian Condo |

SEA CLUB OF HILLSBORO BEA SEA CLUB OF HILLSBORO BEA

|

| Colonial Ridge Corp | REGENCY OF PALM BEACH INC | Coral Ridge Towers Coral Ridge Towers |

| LAKE COLONY APTS TWO INC | Lighthouse Colony Lighthouse Colony | LIGHTHOUSE COLONY CO-OP |

| PEN-TEN APTS INC CO-OP PEN-TEN APTS INC CO-OP | Regency at Boca Pointe | VILLAS ON THE OCEAN |

| Coral Ridge Towers Co-Op Coral Ridge Towers Co-Op | BOULAN SOUTH BEACH CONDO BOULAN SOUTH BEACH CONDO | Sea Tower Sea Tower |

| Coral Ridge Towers Coral Ridge Towers | Atlantic Towers Atlantic Towers |

WOODRIDGE AT CALFORNIA CL WOODRIDGE AT CALFORNIA CL

|

| Coral Ridge Towers East Coral Ridge Towers East | VIA VENTURE NEIGHBORHOOD VIA VENTURE NEIGHBORHOOD | LIGHTHOUSE COVE AT TEQUES |

| Villa Sorrento Villa Sorrento | EDGEWATER ARMS CO-OP | Breakwater Towers Breakwater Towers |

| THE MEADOWS LAKE NORTH CON THE MEADOWS LAKE NORTH CO | ISLE OF PARADISE CO-OP ISLE OF PARADISE | ISLANDER CO-OP ISLANDER CO-OP |

| Cypress Lake East Cypress Lake East | VIRGINIA KAYE CO-OP VIRGINIA KAYE CO-OP |

CORAL RIDGE TOWERS EAST C CORAL RIDGE TOWERS

|

| OPTIMA VILLAGE OPTIMA VILLAGE | ALAQUA CONDO ALAQUA | Coral Ridge Towers Coral Ridge Towers |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | LA FONTANA APTS OF PALM B | PALMBEACHER APTS INC |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Fort Lauderdale Surf Club Fort Lauderdale Surf Club | COLONIAL RIDGE CORP |

| Fairbanks Terrace South Fairbanks Terrace South | Oasis Nurmi Isle |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| BREAKWATER TOWERS CO-OP BREAKWATER TOWERS | CANVAS CONDO CANVAS CONDO | CoralRidge Tower Original CoralRidge Tower Original |

| Lake Mayan Apartments Lake Mayan Apartments | El Dorado Club El Dorado Club | PALMBEACHER |

| MARINE TERRACE CO-OP marine terrace | CORAL RIDGE SOUTH CO-OP CORAL RIDGE SOUTH CO-OP | COLONIAL RIDGE CORP |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Coral Ridge Tower South Coral Ridge Tower South | Breakwater Towers Breakwater Towers |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Spring Tide Apartment Spring Tide Apartment | BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP |

| OCEAN TERRACE CO-OP APTS Ocean Terrace | LAFAYETTE ARMS CO-OP LAFAYETTE ARMS | PARADISE TOWERS CO-OP PARADISE TOWERS |

| ISLE OF PARADISE CO-OP Isle Of Paradise | JAMAICA MANOR INC LESSEE | Coral Ridge Towers South Coral Ridge Towers South |

| Coral Ridge Towers East Coral Ridge Towers East | Ambassador II |

CROSSWINDS APTS INC CO-OP Crosswinds Co-Op Comm

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | OPERA TOWER CONDO OPERA TOWER CONDO |

CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH

|

| Cypress Lake #9 Co-Op Cypress Lake #9 Co-Op | ROYAL SAXON INC | alagon alagon |

| SUNSET VILLAS NO 3 CONDO SUNSET VILLAS CONDO | ATLANTIC TOWERS CO-OP Atlantic Towers | Coral Ridge Towers East Coral Ridge Towers East |

| MARINE TERRACE CO-OP | VIRGINIA KAYE | CARLTON BAY CONDO CARLTON BAY CONDO |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS | Hillsboro Ocean Apts. Hillsboro Ocean Apts. | KING COLE CONDO KING COLE CONDO |

| CASA PARADISO CO-OP Casa Paradiso | Riviera Towers Riviera Towers | ASHLEIGH HOUSE CONDO ASHLEIGH HOUSE CONDO |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | CAPRI CO-OP CAPRI CO-OP | ANDORIC APTS CO-OP Andoric Apartments |

| Coral Ridge Towers East Coral Ridge Towers East | PALMBEACHER APTS INC | CRANE CREST APTS CO-OP Crane Crest |

| CoralRidge Tower Original CoralRidge Tower Original | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP | Coral Ridge Towers Coral Ridge Towers |

| Cypress Island Cypress Island | Coral Ridge Towers North Coral Ridge Towers North | COLONIAL RIDGE CORP |

| W & C CONDO W & C CONDO | 1060 BRICKELL CONDO 1060 Brickell | Silver Shores Silver Shores |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | TAROMINA CO-OP Taromina | SEA COLONY CO-OP SEA COLONY CO-OP |

| THE ESQUIRE HOUSE OF M B THE ESQUIRE CONDO | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Coral Ridge Towers North Coral Ridge Towers North |

| THE ESQUIRE HOUSE OF M B Esquire House of Miami Be | ROYAL SAXON INC | Coral Ridge Towers Coral Ridge Towers |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS CO-OP | AMBASSADOR II | Coral Ridge Towers East Coral Ridge Towers East |

| COASTAL WATERWAYS CO-OP Coastal Waterways | CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH | GLENS CONDO |

| CASA PARADISO CO-OP CASA PARADISO | FOXGLOVE CO-OP FOXGLOVE | IMPERIAL HOUSE INC |

| Q CLUB RESORT & RESIDENCE QClub Resort and Residenc | Edgerwater arms Edgerwater arms | VILLAS ON THE OCEAN |

| Cypress Island Cypress Island | LAMIL SUB Monterey Villas | ROYAL SAXON INC |

| LAKE COLONY APTS THREE IN | REGENCY OF PALM BEACH INC | Atlantic Towers Co-op Atlantic Towers Co-op |

| ANDORIC APARTMENTS ANDORIC APARTMENTS | Estates at Acqualina Estates at Acqualina | MYSTIC POINTE TOWER 500 C Mystic Pointe Tower |

| SEA CLUB OF HILLSBORO BEA | VILLAS INC | Breakwater Towers Breakwater Towers |

| Coral Ridge Towers Coral Ridge Towers | DORCHESTER INC 200 N OCEA | Coral Ridge Towers Coral Ridge Towers |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE EIGHTY NINE CORP LE |

APEX AT PARK CENTRAL COND APEX AT PARK CENTRAL COND

|

| Coral Ridge Towers North Coral Ridge Towers North | Aston Martin Aston Martin Residences | Royal Saxon Inc |

| HILLSBORO MILE OCEAN APTS | THREE EIGHTY NINE CORP LE | Breakwater Towers Breakwater Towers |

| Colonial Ridge Club | SOMERSET OF GULFSTREAM IN | 518 Condo 518 Euclid Av 518 EUCLID |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP | THREE EIGHTY NINE CORP LE |

SIAN OCEAN RESIDENCES CON SIAN OCEAN RESIDENCES

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | PARK PLACE INC | Hawthorne House Hawthorne House |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE HUNDRED SOUTH OCEAN | Caribe Co-Op Caribe Co-Op |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | Coral Ridge Towers East Coral Ridge Towers East |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | THREE EIGHTY NINE CORP LE | SANDPIPER VILLAS CO-OP SANDPIPER VILLAS |

| Coral Ridge Towers South Coral Ridge Towers South | LAKE DRIVE CO-OP APTS INC | Royal Saxon |

| Atlantic Towers Atlantic Towers | MURANO GRANDE AT PORTOFIN Murano Grande | OCEAN CLUB 1 |

| OASIS-NURMI ISLE CO-OP The Oasis | PARK PLACE INC | Coral Ridge Towers East Coral Ridge Towers East |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | ATLANTIC TOWERS CO-OP Atlantic Towers |

| BAY HARBOR CLUB CO-OP Bay Harbor Club Co-Op | The Elser Residences The Elser Residences | SEA CLUB OF HILLSBORO BEA |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | OKAN TOWER OKAN TOWER | Sea Tower Sea Tower |

| Paradise Harbour Paradise Harbour | PARAMOUNT BAY CONDO Paramount Bay | Breakwater Towers Breakwater Towers |

| CORAL COVE CORAL COVE | TWENTY TWO NINETY FIVE SO | Palm Beach Shores Apartme |

| COLONIAL RIDGE CORP | PALM HILL OCEAN CLUB CO-O | Atlantic Towers Atlantic Towers |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | REGENCY OF PALM BEACH INC | Villa Sorrento Villa Sorrento |

| 1446 OCEAN DR CO-OP APTS 1446 OCEAN DR | COVE BEACH CLUB COVE BEACH CLUB | CROSSWINDS CROSSWINDS |

| ISLE OF PARADISE CO-OP ISLE OF PARADISE CO-OP | PALM WORTH INC | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP |

| FAIRBANKS TERRACE SOUTH C FAIRBANKS TERRACE SOUTH C | AMBASSADOR II CORP | Crosswinds Crosswinds |

| CoralRidge Tower Original CoralRidge Tower Original | TWENTY TWO NINETY FIVE SO | Coral Ridge Towers North Coral Ridge Towers North |

| Coral Ridge Towers North Coral Ridge Towers North | Harbour House |

CORAL RIDGE TOWERS EAST Coral Ridge Towers East

|

| LAKEVIEW LODGE CO-OP LAKEVIEW LODGE CO-OP | AMBASSADOR SOUTH DEV CORP | 1750 Las Olas Co-op 1750 Las Olas Co-op |

| PARADISE TOWERS CO-OP Paradise Towers | AMBASSADOR SOUTH DEV CORP | OCEANA SOUTH CONDOMINIUM |

| TIFFANY APTS CO-OP Tiffany Apts Co-Op | AMBASSADOR II CORP | SEA CLUB OF HILLSBORO BEA |

| RIVIERA APTS RIVIERA APTS | ISLAND HOUSE APT INC – CO Island House |

CORAL RIDGE TOWERS CO-OP CORAL RIDGE TOWERS CO-OP

|

| Coral Ridge Towers South Coral Ridge Towers South | FONTAINEBLEAU III OCEAN C SORRENTO | LA FONTANA APTS OF PALM B |

| SHEFFIELD WOODS AT WELLIN Sheffield Woods at Wellin | AMBASSADOR II CORP | CULMER VILLAS CULMER VILLAS PB 106-50 |

| Beach Breeze Beach Breeze | 2295 SOUTH OCEAN BLVD COR | BOCA GRANADA WEST INC |

| BAY HARBOR CLUB CO-OP Bay Harbor Club | THE PLAZA 851 BRICKELL CO The Plaza on Brickell | Coral Ridge Towers East Coral Ridge Towers East |

| COSTA HOLLYWOOD CONDO COSTA HOLLYWOOD CONDO | GROSVENOR HOUSE INC | LEISURE BEACH CONDO LEISURE BEACH CONDO |

| COASTAL WATERWAYS CO-OP Coastal Waterways Co-Op | ISLAND HOUSE APT INC -COOP ISLAND HOUSE APT INC-COOP | LA BONNE VIE CONDO |

| Lexington Arms Co-Op Lexington Arms Co-Op | Old Port Cove – Lake Poin | BREAKWATER TOWERS CO-OP |

| PARADISE HARBOUR APTS CO- Paradise Harbour | AMBASSADOR | Norfolk House Norfolk House |

| Marine Colony Villas Marine Colony Villas | Versailles Versailles | CORAL RIDGE TOWERS EAST C |

| CARIBE CARIBE | REGENCY OF PALM BEACH INC | IMPERIAL WESTBURY CO-OP IMPERIAL WESTBURY |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Delrado | BREAKWATER TOWERS CO-OP Breakwater Towers |

| FAIRBANKS TERRACE SOUTH | Delrado | IMPERIAL HOUSE INC |

| Coral Ridge Towers Coral Ridge Towers | Orleans Chateau & Villas Orleans Chateau & Villas |

HILLSBORO MILE OCEAN APTS HILLSBORO MILE OCEAN APTS

|

| Coral Ridge Towers South Coral Ridge Towers South | VIRGINIA KAYE CO-OP Virginia Kaye | Coral Ridge Towers East Coral Ridge Towers East |

| The Oasis-Nurmi Isle The Oasis-Nurmi Isle | BAL HARBOUR RES SEC Bal Bridge South | EDGEWATER ARMS CO-OP EDGEWATER ARMS CO-OP |

| DELRAY COLONIAL | BURLEIGH HOUSE CONDO Burleigh House | RIVIERA APTS A INC OF HAL Riviera A |

| FAIRBANKS TERRACE SOUTH C Fairbanks Terrace | Cove Beach Club Cove Beach Club | Coral Ridge Towers Coral Ridge Towers |

| KENNEDY HOUSE CONDO KENNEDY HOUSE | Versailles Versailles |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| OCEAN BEACH FLA SUB Balmoral Apartments | TWENTY TWO NINETY FIVE SO | Hawthorne East Hawthorne East |

| GOLDEN BAY TOWERS CO-OP Golden Bay Towers | LEGENDS CONDO | VILLAS ON THE OCEAN |

| COASTAL WATERWAYS CO-OP coastal waterways | GOLDEN BAY TOWERS | OLYMPUS CONDO PHASE Olympus |

| CORAL RIDGE TOWERS CORAL RIDGE TOWERS | 4111 SOUTH OCEAN DRIVE CO 4111 SOUTH OCEAN DRIVE CO | Sea Tower Sea Tower |

| Coral Ridge Towers North Coral Ridge Towers North | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Harbor House Harbor House |

| Coral Ridge Towers Coral Ridge Towers | Spring Tide Apartments Spring Tide Apartments | Atlantic Towers Atlantic Towers |

| Coral Ridge Towers North Coral Ridge Towers North | Venice Venice | OYSTER BAY COOPERATIVE IN |

| ATLANTIC TOWERS ATLANTIC TOWERS | TWENTY TWO NINETY FIVE SO | ATLANTIC TOWERS ATLANTIC TOWERS |

| Breakwater Towers Breakwater Towers | TWENTY TWO NINETY-FIVE SO | Coral Ridge Towers South Coral Ridge Towers South |

| Colonial Ridge Corp | THE MERIDIAN CONDO The Meridian Condo |

SEA CLUB OF HILLSBORO BEA SEA CLUB OF HILLSBORO BEA

|

| Colonial Ridge Corp | REGENCY OF PALM BEACH INC | Coral Ridge Towers Coral Ridge Towers |

| LAKE COLONY APTS TWO INC | Lighthouse Colony Lighthouse Colony | LIGHTHOUSE COLONY CO-OP |

| PEN-TEN APTS INC CO-OP PEN-TEN APTS INC CO-OP | Regency at Boca Pointe | VILLAS ON THE OCEAN |

| Coral Ridge Towers Co-Op Coral Ridge Towers Co-Op | BOULAN SOUTH BEACH CONDO BOULAN SOUTH BEACH CONDO | Sea Tower Sea Tower |

| Coral Ridge Towers Coral Ridge Towers | Atlantic Towers Atlantic Towers |

WOODRIDGE AT CALFORNIA CL WOODRIDGE AT CALFORNIA CL

|

| Coral Ridge Towers East Coral Ridge Towers East | VIA VENTURE NEIGHBORHOOD VIA VENTURE NEIGHBORHOOD | LIGHTHOUSE COVE AT TEQUES |

| Villa Sorrento Villa Sorrento | EDGEWATER ARMS CO-OP | Breakwater Towers Breakwater Towers |

| THE MEADOWS LAKE NORTH CON THE MEADOWS LAKE NORTH CO | ISLE OF PARADISE CO-OP ISLE OF PARADISE | ISLANDER CO-OP ISLANDER CO-OP |

| Cypress Lake East Cypress Lake East | VIRGINIA KAYE CO-OP VIRGINIA KAYE CO-OP |

CORAL RIDGE TOWERS EAST C CORAL RIDGE TOWERS

|

| OPTIMA VILLAGE OPTIMA VILLAGE | ALAQUA CONDO ALAQUA | Coral Ridge Towers Coral Ridge Towers |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | LA FONTANA APTS OF PALM B | PALMBEACHER APTS INC |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Fort Lauderdale Surf Club Fort Lauderdale Surf Club | COLONIAL RIDGE CORP |

| Fairbanks Terrace South Fairbanks Terrace South | Oasis Nurmi Isle |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| BREAKWATER TOWERS CO-OP BREAKWATER TOWERS | CANVAS CONDO CANVAS CONDO | CoralRidge Tower Original CoralRidge Tower Original |

| Lake Mayan Apartments Lake Mayan Apartments | El Dorado Club El Dorado Club | PALMBEACHER |

| MARINE TERRACE CO-OP marine terrace | CORAL RIDGE SOUTH CO-OP CORAL RIDGE SOUTH CO-OP | COLONIAL RIDGE CORP |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Coral Ridge Tower South Coral Ridge Tower South | Breakwater Towers Breakwater Towers |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Spring Tide Apartment Spring Tide Apartment | BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP |

| OCEAN TERRACE CO-OP APTS Ocean Terrace | LAFAYETTE ARMS CO-OP LAFAYETTE ARMS | PARADISE TOWERS CO-OP PARADISE TOWERS |

| ISLE OF PARADISE CO-OP Isle Of Paradise | JAMAICA MANOR INC LESSEE | Coral Ridge Towers South Coral Ridge Towers South |

| Coral Ridge Towers East Coral Ridge Towers East | Ambassador II |

CROSSWINDS APTS INC CO-OP Crosswinds Co-Op Comm

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | OPERA TOWER CONDO OPERA TOWER CONDO |

CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH

|

| Cypress Lake #9 Co-Op Cypress Lake #9 Co-Op | ROYAL SAXON INC | alagon alagon |

| SUNSET VILLAS NO 3 CONDO SUNSET VILLAS CONDO | ATLANTIC TOWERS CO-OP Atlantic Towers | Coral Ridge Towers East Coral Ridge Towers East |

| MARINE TERRACE CO-OP | VIRGINIA KAYE | CARLTON BAY CONDO CARLTON BAY CONDO |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS | Hillsboro Ocean Apts. Hillsboro Ocean Apts. | KING COLE CONDO KING COLE CONDO |

| CASA PARADISO CO-OP Casa Paradiso | Riviera Towers Riviera Towers | ASHLEIGH HOUSE CONDO ASHLEIGH HOUSE CONDO |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | CAPRI CO-OP CAPRI CO-OP | ANDORIC APTS CO-OP Andoric Apartments |

| Coral Ridge Towers East Coral Ridge Towers East | PALMBEACHER APTS INC | CRANE CREST APTS CO-OP Crane Crest |

| CoralRidge Tower Original CoralRidge Tower Original | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP | Coral Ridge Towers Coral Ridge Towers |

| Cypress Island Cypress Island | Coral Ridge Towers North Coral Ridge Towers North | COLONIAL RIDGE CORP |

| W & C CONDO W & C CONDO | 1060 BRICKELL CONDO 1060 Brickell | Silver Shores Silver Shores |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | TAROMINA CO-OP Taromina | SEA COLONY CO-OP SEA COLONY CO-OP |

| THE ESQUIRE HOUSE OF M B THE ESQUIRE CONDO | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Coral Ridge Towers North Coral Ridge Towers North |

| THE ESQUIRE HOUSE OF M B Esquire House of Miami Be | ROYAL SAXON INC | Coral Ridge Towers Coral Ridge Towers |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS CO-OP | AMBASSADOR II | Coral Ridge Towers East Coral Ridge Towers East |

| COASTAL WATERWAYS CO-OP Coastal Waterways | CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH | GLENS CONDO |

| CASA PARADISO CO-OP CASA PARADISO | FOXGLOVE CO-OP FOXGLOVE | IMPERIAL HOUSE INC |

| Q CLUB RESORT & RESIDENCE QClub Resort and Residenc | Edgerwater arms Edgerwater arms | VILLAS ON THE OCEAN |

| Cypress Island Cypress Island | LAMIL SUB Monterey Villas | ROYAL SAXON INC |

| LAKE COLONY APTS THREE IN | REGENCY OF PALM BEACH INC | Atlantic Towers Co-op Atlantic Towers Co-op |

| ANDORIC APARTMENTS ANDORIC APARTMENTS | Estates at Acqualina Estates at Acqualina | MYSTIC POINTE TOWER 500 C Mystic Pointe Tower |

| SEA CLUB OF HILLSBORO BEA | VILLAS INC | Breakwater Towers Breakwater Towers |

| Coral Ridge Towers Coral Ridge Towers | DORCHESTER INC 200 N OCEA | Coral Ridge Towers Coral Ridge Towers |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE EIGHTY NINE CORP LE |

APEX AT PARK CENTRAL COND APEX AT PARK CENTRAL COND

|

| Coral Ridge Towers North Coral Ridge Towers North | Aston Martin Aston Martin Residences | Royal Saxon Inc |

| HILLSBORO MILE OCEAN APTS | THREE EIGHTY NINE CORP LE | Breakwater Towers Breakwater Towers |

| Colonial Ridge Club | SOMERSET OF GULFSTREAM IN | 518 Condo 518 Euclid Av 518 EUCLID |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP | THREE EIGHTY NINE CORP LE |

SIAN OCEAN RESIDENCES CON SIAN OCEAN RESIDENCES

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | PARK PLACE INC | Hawthorne House Hawthorne House |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE HUNDRED SOUTH OCEAN | Caribe Co-Op Caribe Co-Op |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | Coral Ridge Towers East Coral Ridge Towers East |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | THREE EIGHTY NINE CORP LE | SANDPIPER VILLAS CO-OP SANDPIPER VILLAS |

| Coral Ridge Towers South Coral Ridge Towers South | LAKE DRIVE CO-OP APTS INC | Royal Saxon |

| Atlantic Towers Atlantic Towers | MURANO GRANDE AT PORTOFIN Murano Grande | OCEAN CLUB 1 |

| OASIS-NURMI ISLE CO-OP The Oasis | PARK PLACE INC | Coral Ridge Towers East Coral Ridge Towers East |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | ATLANTIC TOWERS CO-OP Atlantic Towers |

| BAY HARBOR CLUB CO-OP Bay Harbor Club Co-Op | The Elser Residences The Elser Residences | SEA CLUB OF HILLSBORO BEA |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | OKAN TOWER OKAN TOWER | Sea Tower Sea Tower |

| Paradise Harbour Paradise Harbour | PARAMOUNT BAY CONDO Paramount Bay | Breakwater Towers Breakwater Towers |

| CORAL COVE CORAL COVE | TWENTY TWO NINETY FIVE SO | Palm Beach Shores Apartme |

| COLONIAL RIDGE CORP | PALM HILL OCEAN CLUB CO-O | Atlantic Towers Atlantic Towers |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | REGENCY OF PALM BEACH INC | Villa Sorrento Villa Sorrento |

| 1446 OCEAN DR CO-OP APTS 1446 OCEAN DR | COVE BEACH CLUB COVE BEACH CLUB | CROSSWINDS CROSSWINDS |

| ISLE OF PARADISE CO-OP ISLE OF PARADISE CO-OP | PALM WORTH INC | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP |

| FAIRBANKS TERRACE SOUTH C FAIRBANKS TERRACE SOUTH C | AMBASSADOR II CORP | Crosswinds Crosswinds |

| CoralRidge Tower Original CoralRidge Tower Original | TWENTY TWO NINETY FIVE SO | Coral Ridge Towers North Coral Ridge Towers North |

| Coral Ridge Towers North Coral Ridge Towers North | Harbour House |

CORAL RIDGE TOWERS EAST Coral Ridge Towers East

|

| LAKEVIEW LODGE CO-OP LAKEVIEW LODGE CO-OP | AMBASSADOR SOUTH DEV CORP | 1750 Las Olas Co-op 1750 Las Olas Co-op |

| PARADISE TOWERS CO-OP Paradise Towers | AMBASSADOR SOUTH DEV CORP | OCEANA SOUTH CONDOMINIUM |

| TIFFANY APTS CO-OP Tiffany Apts Co-Op | AMBASSADOR II CORP | SEA CLUB OF HILLSBORO BEA |

| RIVIERA APTS RIVIERA APTS | ISLAND HOUSE APT INC – CO Island House |

CORAL RIDGE TOWERS CO-OP CORAL RIDGE TOWERS CO-OP

|

| Coral Ridge Towers South Coral Ridge Towers South | FONTAINEBLEAU III OCEAN C SORRENTO | LA FONTANA APTS OF PALM B |

| SHEFFIELD WOODS AT WELLIN Sheffield Woods at Wellin | AMBASSADOR II CORP | CULMER VILLAS CULMER VILLAS PB 106-50 |

| Beach Breeze Beach Breeze | 2295 SOUTH OCEAN BLVD COR | BOCA GRANADA WEST INC |

| BAY HARBOR CLUB CO-OP Bay Harbor Club | THE PLAZA 851 BRICKELL CO The Plaza on Brickell | Coral Ridge Towers East Coral Ridge Towers East |

| COSTA HOLLYWOOD CONDO COSTA HOLLYWOOD CONDO | GROSVENOR HOUSE INC | LEISURE BEACH CONDO LEISURE BEACH CONDO |

| COASTAL WATERWAYS CO-OP Coastal Waterways Co-Op | ISLAND HOUSE APT INC -COOP ISLAND HOUSE APT INC-COOP | LA BONNE VIE CONDO |

| Lexington Arms Co-Op Lexington Arms Co-Op | Old Port Cove – Lake Poin | BREAKWATER TOWERS CO-OP |

| PARADISE HARBOUR APTS CO- Paradise Harbour | AMBASSADOR | Norfolk House Norfolk House |

| Marine Colony Villas Marine Colony Villas | Versailles Versailles | CORAL RIDGE TOWERS EAST C |

| CARIBE CARIBE | REGENCY OF PALM BEACH INC | IMPERIAL WESTBURY CO-OP IMPERIAL WESTBURY |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Delrado | BREAKWATER TOWERS CO-OP Breakwater Towers |

| FAIRBANKS TERRACE SOUTH | Delrado | IMPERIAL HOUSE INC |

| Coral Ridge Towers Coral Ridge Towers | Orleans Chateau & Villas Orleans Chateau & Villas |

HILLSBORO MILE OCEAN APTS HILLSBORO MILE OCEAN APTS

|

| Coral Ridge Towers South Coral Ridge Towers South | VIRGINIA KAYE CO-OP Virginia Kaye | Coral Ridge Towers East Coral Ridge Towers East |

| The Oasis-Nurmi Isle The Oasis-Nurmi Isle | BAL HARBOUR RES SEC Bal Bridge South | EDGEWATER ARMS CO-OP EDGEWATER ARMS CO-OP |

| DELRAY COLONIAL | BURLEIGH HOUSE CONDO Burleigh House | RIVIERA APTS A INC OF HAL Riviera A |

| FAIRBANKS TERRACE SOUTH C Fairbanks Terrace | Cove Beach Club Cove Beach Club | Coral Ridge Towers Coral Ridge Towers |

| KENNEDY HOUSE CONDO KENNEDY HOUSE | Versailles Versailles |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| OCEAN BEACH FLA SUB Balmoral Apartments | TWENTY TWO NINETY FIVE SO | Hawthorne East Hawthorne East |

| GOLDEN BAY TOWERS CO-OP Golden Bay Towers | LEGENDS CONDO | VILLAS ON THE OCEAN |

| COASTAL WATERWAYS CO-OP coastal waterways | GOLDEN BAY TOWERS | OLYMPUS CONDO PHASE Olympus |

| CORAL RIDGE TOWERS CORAL RIDGE TOWERS | 4111 SOUTH OCEAN DRIVE CO 4111 SOUTH OCEAN DRIVE CO | Sea Tower Sea Tower |

| Coral Ridge Towers North Coral Ridge Towers North | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Harbor House Harbor House |

| Coral Ridge Towers Coral Ridge Towers | Spring Tide Apartments Spring Tide Apartments | Atlantic Towers Atlantic Towers |

| Coral Ridge Towers North Coral Ridge Towers North | Venice Venice | OYSTER BAY COOPERATIVE IN |

| ATLANTIC TOWERS ATLANTIC TOWERS | TWENTY TWO NINETY FIVE SO | ATLANTIC TOWERS ATLANTIC TOWERS |

| Breakwater Towers Breakwater Towers | TWENTY TWO NINETY-FIVE SO | Coral Ridge Towers South Coral Ridge Towers South |

| Colonial Ridge Corp | THE MERIDIAN CONDO The Meridian Condo |

SEA CLUB OF HILLSBORO BEA SEA CLUB OF HILLSBORO BEA

|

| Colonial Ridge Corp | REGENCY OF PALM BEACH INC | Coral Ridge Towers Coral Ridge Towers |

| LAKE COLONY APTS TWO INC | Lighthouse Colony Lighthouse Colony | LIGHTHOUSE COLONY CO-OP |

| PEN-TEN APTS INC CO-OP PEN-TEN APTS INC CO-OP | Regency at Boca Pointe | VILLAS ON THE OCEAN |

| Coral Ridge Towers Co-Op Coral Ridge Towers Co-Op | BOULAN SOUTH BEACH CONDO BOULAN SOUTH BEACH CONDO | Sea Tower Sea Tower |

| Coral Ridge Towers Coral Ridge Towers | Atlantic Towers Atlantic Towers |

WOODRIDGE AT CALFORNIA CL WOODRIDGE AT CALFORNIA CL

|

| Coral Ridge Towers East Coral Ridge Towers East | VIA VENTURE NEIGHBORHOOD VIA VENTURE NEIGHBORHOOD | LIGHTHOUSE COVE AT TEQUES |

| Villa Sorrento Villa Sorrento | EDGEWATER ARMS CO-OP | Breakwater Towers Breakwater Towers |

| THE MEADOWS LAKE NORTH CON THE MEADOWS LAKE NORTH CO | ISLE OF PARADISE CO-OP ISLE OF PARADISE | ISLANDER CO-OP ISLANDER CO-OP |

| Cypress Lake East Cypress Lake East | VIRGINIA KAYE CO-OP VIRGINIA KAYE CO-OP |

CORAL RIDGE TOWERS EAST C CORAL RIDGE TOWERS

|

| OPTIMA VILLAGE OPTIMA VILLAGE | ALAQUA CONDO ALAQUA | Coral Ridge Towers Coral Ridge Towers |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | LA FONTANA APTS OF PALM B | PALMBEACHER APTS INC |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Fort Lauderdale Surf Club Fort Lauderdale Surf Club | COLONIAL RIDGE CORP |

| Fairbanks Terrace South Fairbanks Terrace South | Oasis Nurmi Isle |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| BREAKWATER TOWERS CO-OP BREAKWATER TOWERS | CANVAS CONDO CANVAS CONDO | CoralRidge Tower Original CoralRidge Tower Original |

| Lake Mayan Apartments Lake Mayan Apartments | El Dorado Club El Dorado Club | PALMBEACHER |

| MARINE TERRACE CO-OP marine terrace | CORAL RIDGE SOUTH CO-OP CORAL RIDGE SOUTH CO-OP | COLONIAL RIDGE CORP |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Coral Ridge Tower South Coral Ridge Tower South | Breakwater Towers Breakwater Towers |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Spring Tide Apartment Spring Tide Apartment | BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP |

| OCEAN TERRACE CO-OP APTS Ocean Terrace | LAFAYETTE ARMS CO-OP LAFAYETTE ARMS | PARADISE TOWERS CO-OP PARADISE TOWERS |

| ISLE OF PARADISE CO-OP Isle Of Paradise | JAMAICA MANOR INC LESSEE | Coral Ridge Towers South Coral Ridge Towers South |

| Coral Ridge Towers East Coral Ridge Towers East | Ambassador II |

CROSSWINDS APTS INC CO-OP Crosswinds Co-Op Comm

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | OPERA TOWER CONDO OPERA TOWER CONDO |

CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH

|

| Cypress Lake #9 Co-Op Cypress Lake #9 Co-Op | ROYAL SAXON INC | alagon alagon |

| SUNSET VILLAS NO 3 CONDO SUNSET VILLAS CONDO | ATLANTIC TOWERS CO-OP Atlantic Towers | Coral Ridge Towers East Coral Ridge Towers East |

| MARINE TERRACE CO-OP | VIRGINIA KAYE | CARLTON BAY CONDO CARLTON BAY CONDO |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS | Hillsboro Ocean Apts. Hillsboro Ocean Apts. | KING COLE CONDO KING COLE CONDO |

| CASA PARADISO CO-OP Casa Paradiso | Riviera Towers Riviera Towers | ASHLEIGH HOUSE CONDO ASHLEIGH HOUSE CONDO |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | CAPRI CO-OP CAPRI CO-OP | ANDORIC APTS CO-OP Andoric Apartments |

| Coral Ridge Towers East Coral Ridge Towers East | PALMBEACHER APTS INC | CRANE CREST APTS CO-OP Crane Crest |

| CoralRidge Tower Original CoralRidge Tower Original | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP | Coral Ridge Towers Coral Ridge Towers |

| Cypress Island Cypress Island | Coral Ridge Towers North Coral Ridge Towers North | COLONIAL RIDGE CORP |

| W & C CONDO W & C CONDO | 1060 BRICKELL CONDO 1060 Brickell | Silver Shores Silver Shores |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | TAROMINA CO-OP Taromina | SEA COLONY CO-OP SEA COLONY CO-OP |

| THE ESQUIRE HOUSE OF M B THE ESQUIRE CONDO | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Coral Ridge Towers North Coral Ridge Towers North |

| THE ESQUIRE HOUSE OF M B Esquire House of Miami Be | ROYAL SAXON INC | Coral Ridge Towers Coral Ridge Towers |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS CO-OP | AMBASSADOR II | Coral Ridge Towers East Coral Ridge Towers East |

| COASTAL WATERWAYS CO-OP Coastal Waterways | CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH | GLENS CONDO |

| CASA PARADISO CO-OP CASA PARADISO | FOXGLOVE CO-OP FOXGLOVE | IMPERIAL HOUSE INC |

| Q CLUB RESORT & RESIDENCE QClub Resort and Residenc | Edgerwater arms Edgerwater arms | VILLAS ON THE OCEAN |

| Cypress Island Cypress Island | LAMIL SUB Monterey Villas | ROYAL SAXON INC |

| LAKE COLONY APTS THREE IN | REGENCY OF PALM BEACH INC | Atlantic Towers Co-op Atlantic Towers Co-op |

| ANDORIC APARTMENTS ANDORIC APARTMENTS | Estates at Acqualina Estates at Acqualina | MYSTIC POINTE TOWER 500 C Mystic Pointe Tower |

| SEA CLUB OF HILLSBORO BEA | VILLAS INC | Breakwater Towers Breakwater Towers |

| Coral Ridge Towers Coral Ridge Towers | DORCHESTER INC 200 N OCEA | Coral Ridge Towers Coral Ridge Towers |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE EIGHTY NINE CORP LE |

APEX AT PARK CENTRAL COND APEX AT PARK CENTRAL COND

|

| Coral Ridge Towers North Coral Ridge Towers North | Aston Martin Aston Martin Residences | Royal Saxon Inc |

| HILLSBORO MILE OCEAN APTS | THREE EIGHTY NINE CORP LE | Breakwater Towers Breakwater Towers |

| Colonial Ridge Club | SOMERSET OF GULFSTREAM IN | 518 Condo 518 Euclid Av 518 EUCLID |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP | THREE EIGHTY NINE CORP LE |

SIAN OCEAN RESIDENCES CON SIAN OCEAN RESIDENCES

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | PARK PLACE INC | Hawthorne House Hawthorne House |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE HUNDRED SOUTH OCEAN | Caribe Co-Op Caribe Co-Op |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | Coral Ridge Towers East Coral Ridge Towers East |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | THREE EIGHTY NINE CORP LE | SANDPIPER VILLAS CO-OP SANDPIPER VILLAS |

| Coral Ridge Towers South Coral Ridge Towers South | LAKE DRIVE CO-OP APTS INC | Royal Saxon |

| Atlantic Towers Atlantic Towers | MURANO GRANDE AT PORTOFIN Murano Grande | OCEAN CLUB 1 |

| OASIS-NURMI ISLE CO-OP The Oasis | PARK PLACE INC | Coral Ridge Towers East Coral Ridge Towers East |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | ATLANTIC TOWERS CO-OP Atlantic Towers |

| BAY HARBOR CLUB CO-OP Bay Harbor Club Co-Op | The Elser Residences The Elser Residences | SEA CLUB OF HILLSBORO BEA |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | OKAN TOWER OKAN TOWER | Sea Tower Sea Tower |

| Paradise Harbour Paradise Harbour | PARAMOUNT BAY CONDO Paramount Bay | Breakwater Towers Breakwater Towers |

| CORAL COVE CORAL COVE | TWENTY TWO NINETY FIVE SO | Palm Beach Shores Apartme |

| COLONIAL RIDGE CORP | PALM HILL OCEAN CLUB CO-O | Atlantic Towers Atlantic Towers |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | REGENCY OF PALM BEACH INC | Villa Sorrento Villa Sorrento |

| 1446 OCEAN DR CO-OP APTS 1446 OCEAN DR | COVE BEACH CLUB COVE BEACH CLUB | CROSSWINDS CROSSWINDS |

| ISLE OF PARADISE CO-OP ISLE OF PARADISE CO-OP | PALM WORTH INC | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP |

| FAIRBANKS TERRACE SOUTH C FAIRBANKS TERRACE SOUTH C | AMBASSADOR II CORP | Crosswinds Crosswinds |

| CoralRidge Tower Original CoralRidge Tower Original | TWENTY TWO NINETY FIVE SO | Coral Ridge Towers North Coral Ridge Towers North |

| Coral Ridge Towers North Coral Ridge Towers North | Harbour House |

CORAL RIDGE TOWERS EAST Coral Ridge Towers East

|

| LAKEVIEW LODGE CO-OP LAKEVIEW LODGE CO-OP | AMBASSADOR SOUTH DEV CORP | 1750 Las Olas Co-op 1750 Las Olas Co-op |

| PARADISE TOWERS CO-OP Paradise Towers | AMBASSADOR SOUTH DEV CORP | OCEANA SOUTH CONDOMINIUM |

| TIFFANY APTS CO-OP Tiffany Apts Co-Op | AMBASSADOR II CORP | SEA CLUB OF HILLSBORO BEA |

| RIVIERA APTS RIVIERA APTS | ISLAND HOUSE APT INC – CO Island House |

CORAL RIDGE TOWERS CO-OP CORAL RIDGE TOWERS CO-OP

|

| Coral Ridge Towers South Coral Ridge Towers South | FONTAINEBLEAU III OCEAN C SORRENTO | LA FONTANA APTS OF PALM B |

| SHEFFIELD WOODS AT WELLIN Sheffield Woods at Wellin | AMBASSADOR II CORP | CULMER VILLAS CULMER VILLAS PB 106-50 |

| Beach Breeze Beach Breeze | 2295 SOUTH OCEAN BLVD COR | BOCA GRANADA WEST INC |

| BAY HARBOR CLUB CO-OP Bay Harbor Club | THE PLAZA 851 BRICKELL CO The Plaza on Brickell | Coral Ridge Towers East Coral Ridge Towers East |

| COSTA HOLLYWOOD CONDO COSTA HOLLYWOOD CONDO | GROSVENOR HOUSE INC | LEISURE BEACH CONDO LEISURE BEACH CONDO |

| COASTAL WATERWAYS CO-OP Coastal Waterways Co-Op | ISLAND HOUSE APT INC -COOP ISLAND HOUSE APT INC-COOP | LA BONNE VIE CONDO |

| Lexington Arms Co-Op Lexington Arms Co-Op | Old Port Cove – Lake Poin | BREAKWATER TOWERS CO-OP |

| PARADISE HARBOUR APTS CO- Paradise Harbour | AMBASSADOR | Norfolk House Norfolk House |

| Marine Colony Villas Marine Colony Villas | Versailles Versailles | CORAL RIDGE TOWERS EAST C |

| CARIBE CARIBE | REGENCY OF PALM BEACH INC | IMPERIAL WESTBURY CO-OP IMPERIAL WESTBURY |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Delrado | BREAKWATER TOWERS CO-OP Breakwater Towers |

| FAIRBANKS TERRACE SOUTH | Delrado | IMPERIAL HOUSE INC |

| Coral Ridge Towers Coral Ridge Towers | Orleans Chateau & Villas Orleans Chateau & Villas |

HILLSBORO MILE OCEAN APTS HILLSBORO MILE OCEAN APTS

|

| Coral Ridge Towers South Coral Ridge Towers South | VIRGINIA KAYE CO-OP Virginia Kaye | Coral Ridge Towers East Coral Ridge Towers East |

| The Oasis-Nurmi Isle The Oasis-Nurmi Isle | BAL HARBOUR RES SEC Bal Bridge South | EDGEWATER ARMS CO-OP EDGEWATER ARMS CO-OP |

| DELRAY COLONIAL | BURLEIGH HOUSE CONDO Burleigh House | RIVIERA APTS A INC OF HAL Riviera A |

| FAIRBANKS TERRACE SOUTH C Fairbanks Terrace | Cove Beach Club Cove Beach Club | Coral Ridge Towers Coral Ridge Towers |

| KENNEDY HOUSE CONDO KENNEDY HOUSE | Versailles Versailles |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| OCEAN BEACH FLA SUB Balmoral Apartments | TWENTY TWO NINETY FIVE SO | Hawthorne East Hawthorne East |

| GOLDEN BAY TOWERS CO-OP Golden Bay Towers | LEGENDS CONDO | VILLAS ON THE OCEAN |

| COASTAL WATERWAYS CO-OP coastal waterways | GOLDEN BAY TOWERS | OLYMPUS CONDO PHASE Olympus |

| CORAL RIDGE TOWERS CORAL RIDGE TOWERS | 4111 SOUTH OCEAN DRIVE CO 4111 SOUTH OCEAN DRIVE CO | Sea Tower Sea Tower |

| Coral Ridge Towers North Coral Ridge Towers North | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Harbor House Harbor House |

| Coral Ridge Towers Coral Ridge Towers | Spring Tide Apartments Spring Tide Apartments | Atlantic Towers Atlantic Towers |

| Coral Ridge Towers North Coral Ridge Towers North | Venice Venice | OYSTER BAY COOPERATIVE IN |

| ATLANTIC TOWERS ATLANTIC TOWERS | TWENTY TWO NINETY FIVE SO | ATLANTIC TOWERS ATLANTIC TOWERS |

| Breakwater Towers Breakwater Towers | TWENTY TWO NINETY-FIVE SO | Coral Ridge Towers South Coral Ridge Towers South |

| Colonial Ridge Corp | THE MERIDIAN CONDO The Meridian Condo |

SEA CLUB OF HILLSBORO BEA SEA CLUB OF HILLSBORO BEA

|

| Colonial Ridge Corp | REGENCY OF PALM BEACH INC | Coral Ridge Towers Coral Ridge Towers |

| LAKE COLONY APTS TWO INC | Lighthouse Colony Lighthouse Colony | LIGHTHOUSE COLONY CO-OP |

| PEN-TEN APTS INC CO-OP PEN-TEN APTS INC CO-OP | Regency at Boca Pointe | VILLAS ON THE OCEAN |

| Coral Ridge Towers Co-Op Coral Ridge Towers Co-Op | BOULAN SOUTH BEACH CONDO BOULAN SOUTH BEACH CONDO | Sea Tower Sea Tower |

| Coral Ridge Towers Coral Ridge Towers | Atlantic Towers Atlantic Towers |

WOODRIDGE AT CALFORNIA CL WOODRIDGE AT CALFORNIA CL

|

| Coral Ridge Towers East Coral Ridge Towers East | VIA VENTURE NEIGHBORHOOD VIA VENTURE NEIGHBORHOOD | LIGHTHOUSE COVE AT TEQUES |

| Villa Sorrento Villa Sorrento | EDGEWATER ARMS CO-OP | Breakwater Towers Breakwater Towers |

| THE MEADOWS LAKE NORTH CON THE MEADOWS LAKE NORTH CO | ISLE OF PARADISE CO-OP ISLE OF PARADISE | ISLANDER CO-OP ISLANDER CO-OP |

| Cypress Lake East Cypress Lake East | VIRGINIA KAYE CO-OP VIRGINIA KAYE CO-OP |

CORAL RIDGE TOWERS EAST C CORAL RIDGE TOWERS

|

| OPTIMA VILLAGE OPTIMA VILLAGE | ALAQUA CONDO ALAQUA | Coral Ridge Towers Coral Ridge Towers |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | LA FONTANA APTS OF PALM B | PALMBEACHER APTS INC |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Fort Lauderdale Surf Club Fort Lauderdale Surf Club | COLONIAL RIDGE CORP |

| Fairbanks Terrace South Fairbanks Terrace South | Oasis Nurmi Isle |

CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH

|

| BREAKWATER TOWERS CO-OP BREAKWATER TOWERS | CANVAS CONDO CANVAS CONDO | CoralRidge Tower Original CoralRidge Tower Original |

| Lake Mayan Apartments Lake Mayan Apartments | El Dorado Club El Dorado Club | PALMBEACHER |

| MARINE TERRACE CO-OP marine terrace | CORAL RIDGE SOUTH CO-OP CORAL RIDGE SOUTH CO-OP | COLONIAL RIDGE CORP |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Coral Ridge Tower South Coral Ridge Tower South | Breakwater Towers Breakwater Towers |

| OCEAN BEACH FLA SUB OCEAN TOWERS INC | Spring Tide Apartment Spring Tide Apartment | BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP |

| OCEAN TERRACE CO-OP APTS Ocean Terrace | LAFAYETTE ARMS CO-OP LAFAYETTE ARMS | PARADISE TOWERS CO-OP PARADISE TOWERS |

| ISLE OF PARADISE CO-OP Isle Of Paradise | JAMAICA MANOR INC LESSEE | Coral Ridge Towers South Coral Ridge Towers South |

| Coral Ridge Towers East Coral Ridge Towers East | Ambassador II |

CROSSWINDS APTS INC CO-OP Crosswinds Co-Op Comm

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | OPERA TOWER CONDO OPERA TOWER CONDO |

CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH

|

| Cypress Lake #9 Co-Op Cypress Lake #9 Co-Op | ROYAL SAXON INC | alagon alagon |

| SUNSET VILLAS NO 3 CONDO SUNSET VILLAS CONDO | ATLANTIC TOWERS CO-OP Atlantic Towers | Coral Ridge Towers East Coral Ridge Towers East |

| MARINE TERRACE CO-OP | VIRGINIA KAYE | CARLTON BAY CONDO CARLTON BAY CONDO |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS | Hillsboro Ocean Apts. Hillsboro Ocean Apts. | KING COLE CONDO KING COLE CONDO |

| CASA PARADISO CO-OP Casa Paradiso | Riviera Towers Riviera Towers | ASHLEIGH HOUSE CONDO ASHLEIGH HOUSE CONDO |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | CAPRI CO-OP CAPRI CO-OP | ANDORIC APTS CO-OP Andoric Apartments |

| Coral Ridge Towers East Coral Ridge Towers East | PALMBEACHER APTS INC | CRANE CREST APTS CO-OP Crane Crest |

| CoralRidge Tower Original CoralRidge Tower Original | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP | Coral Ridge Towers Coral Ridge Towers |

| Cypress Island Cypress Island | Coral Ridge Towers North Coral Ridge Towers North | COLONIAL RIDGE CORP |

| W & C CONDO W & C CONDO | 1060 BRICKELL CONDO 1060 Brickell | Silver Shores Silver Shores |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | TAROMINA CO-OP Taromina | SEA COLONY CO-OP SEA COLONY CO-OP |

| THE ESQUIRE HOUSE OF M B THE ESQUIRE CONDO | CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Coral Ridge Towers North Coral Ridge Towers North |

| THE ESQUIRE HOUSE OF M B Esquire House of Miami Be | ROYAL SAXON INC | Coral Ridge Towers Coral Ridge Towers |

| COASTAL WATERWAYS CO-OP COASTAL WATERWAYS CO-OP | AMBASSADOR II | Coral Ridge Towers East Coral Ridge Towers East |

| COASTAL WATERWAYS CO-OP Coastal Waterways | CORAL RIDGE TOWERS SOUTH CORAL RIDGE TOWERS SOUTH | GLENS CONDO |

| CASA PARADISO CO-OP CASA PARADISO | FOXGLOVE CO-OP FOXGLOVE | IMPERIAL HOUSE INC |

| Q CLUB RESORT & RESIDENCE QClub Resort and Residenc | Edgerwater arms Edgerwater arms | VILLAS ON THE OCEAN |

| Cypress Island Cypress Island | LAMIL SUB Monterey Villas | ROYAL SAXON INC |

| LAKE COLONY APTS THREE IN | REGENCY OF PALM BEACH INC | Atlantic Towers Co-op Atlantic Towers Co-op |

| ANDORIC APARTMENTS ANDORIC APARTMENTS | Estates at Acqualina Estates at Acqualina | MYSTIC POINTE TOWER 500 C Mystic Pointe Tower |

| SEA CLUB OF HILLSBORO BEA | VILLAS INC | Breakwater Towers Breakwater Towers |

| Coral Ridge Towers Coral Ridge Towers | DORCHESTER INC 200 N OCEA | Coral Ridge Towers Coral Ridge Towers |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE EIGHTY NINE CORP LE |

APEX AT PARK CENTRAL COND APEX AT PARK CENTRAL COND

|

| Coral Ridge Towers North Coral Ridge Towers North | Aston Martin Aston Martin Residences | Royal Saxon Inc |

| HILLSBORO MILE OCEAN APTS | THREE EIGHTY NINE CORP LE | Breakwater Towers Breakwater Towers |

| Colonial Ridge Club | SOMERSET OF GULFSTREAM IN | 518 Condo 518 Euclid Av 518 EUCLID |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB CO-OP | THREE EIGHTY NINE CORP LE |

SIAN OCEAN RESIDENCES CON SIAN OCEAN RESIDENCES

|

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | PARK PLACE INC | Hawthorne House Hawthorne House |

| Cypress Lake East Co-Op Cypress Lake East Co-Op | THREE HUNDRED SOUTH OCEAN | Caribe Co-Op Caribe Co-Op |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | Coral Ridge Towers East Coral Ridge Towers East |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS | THREE EIGHTY NINE CORP LE | SANDPIPER VILLAS CO-OP SANDPIPER VILLAS |

| Coral Ridge Towers South Coral Ridge Towers South | LAKE DRIVE CO-OP APTS INC | Royal Saxon |

| Atlantic Towers Atlantic Towers | MURANO GRANDE AT PORTOFIN Murano Grande | OCEAN CLUB 1 |

| OASIS-NURMI ISLE CO-OP The Oasis | PARK PLACE INC | Coral Ridge Towers East Coral Ridge Towers East |

| LAKESIDE DRIVE APTS INC | THREE EIGHTY NINE CORP LE | ATLANTIC TOWERS CO-OP Atlantic Towers |

| BAY HARBOR CLUB CO-OP Bay Harbor Club Co-Op | The Elser Residences The Elser Residences | SEA CLUB OF HILLSBORO BEA |

| BAY HARBOR CLUB CO-OP BAY HARBOR CLUB | OKAN TOWER OKAN TOWER | Sea Tower Sea Tower |

| Paradise Harbour Paradise Harbour | PARAMOUNT BAY CONDO Paramount Bay | Breakwater Towers Breakwater Towers |

| CORAL COVE CORAL COVE | TWENTY TWO NINETY FIVE SO | Palm Beach Shores Apartme |

| COLONIAL RIDGE CORP | PALM HILL OCEAN CLUB CO-O | Atlantic Towers Atlantic Towers |

| ATLANTIC TOWERS CO-OP ATLANTIC TOWERS CO-OP | REGENCY OF PALM BEACH INC | Villa Sorrento Villa Sorrento |

| 1446 OCEAN DR CO-OP APTS 1446 OCEAN DR | COVE BEACH CLUB COVE BEACH CLUB | CROSSWINDS CROSSWINDS |

| ISLE OF PARADISE CO-OP ISLE OF PARADISE CO-OP | PALM WORTH INC | COVE BEACH CLUB CO-OP COVE BEACH CLUB CO-OP |

| FAIRBANKS TERRACE SOUTH C FAIRBANKS TERRACE SOUTH C | AMBASSADOR II CORP | Crosswinds Crosswinds |

| CoralRidge Tower Original CoralRidge Tower Original | TWENTY TWO NINETY FIVE SO | Coral Ridge Towers North Coral Ridge Towers North |

| Coral Ridge Towers North Coral Ridge Towers North | Harbour House |

CORAL RIDGE TOWERS EAST Coral Ridge Towers East

|

| LAKEVIEW LODGE CO-OP LAKEVIEW LODGE CO-OP | AMBASSADOR SOUTH DEV CORP | 1750 Las Olas Co-op 1750 Las Olas Co-op |

| PARADISE TOWERS CO-OP Paradise Towers | AMBASSADOR SOUTH DEV CORP | OCEANA SOUTH CONDOMINIUM |

| TIFFANY APTS CO-OP Tiffany Apts Co-Op | AMBASSADOR II CORP | SEA CLUB OF HILLSBORO BEA |

| RIVIERA APTS RIVIERA APTS | ISLAND HOUSE APT INC – CO Island House |

CORAL RIDGE TOWERS CO-OP CORAL RIDGE TOWERS CO-OP

|

| Coral Ridge Towers South Coral Ridge Towers South | FONTAINEBLEAU III OCEAN C SORRENTO | LA FONTANA APTS OF PALM B |

| SHEFFIELD WOODS AT WELLIN Sheffield Woods at Wellin | AMBASSADOR II CORP | CULMER VILLAS CULMER VILLAS PB 106-50 |

| Beach Breeze Beach Breeze | 2295 SOUTH OCEAN BLVD COR | BOCA GRANADA WEST INC |

| BAY HARBOR CLUB CO-OP Bay Harbor Club | THE PLAZA 851 BRICKELL CO The Plaza on Brickell | Coral Ridge Towers East Coral Ridge Towers East |

| COSTA HOLLYWOOD CONDO COSTA HOLLYWOOD CONDO | GROSVENOR HOUSE INC | LEISURE BEACH CONDO LEISURE BEACH CONDO |

| COASTAL WATERWAYS CO-OP Coastal Waterways Co-Op | ISLAND HOUSE APT INC -COOP ISLAND HOUSE APT INC-COOP | LA BONNE VIE CONDO |

| Lexington Arms Co-Op Lexington Arms Co-Op | Old Port Cove – Lake Poin | BREAKWATER TOWERS CO-OP |

| PARADISE HARBOUR APTS CO- Paradise Harbour | AMBASSADOR | Norfolk House Norfolk House |

| Marine Colony Villas Marine Colony Villas | Versailles Versailles | CORAL RIDGE TOWERS EAST C |

| CARIBE CARIBE | REGENCY OF PALM BEACH INC | IMPERIAL WESTBURY CO-OP IMPERIAL WESTBURY |

| CORAL RIDGE TOWERS NORTH CORAL RIDGE TOWERS NORTH | Delrado | BREAKWATER TOWERS CO-OP Breakwater Towers |